Deposit rates unlikely to rise in next few quarters

After two years of declining returns, a key question troubling Indian savers and pensioners is – are deposit rates going up anytime soon? The answer is no. In fact, rising inflation could further eat into returns in the months ahead. As of this past February, a one-year term deposit fetched an average 5.20 per cent […]

After two years of declining returns, a key question troubling Indian savers and pensioners is – are deposit rates going up anytime soon? The answer is no. In fact, rising inflation could further eat into returns in the months ahead.

As of this past February, a one-year term deposit fetched an average 5.20 per cent interest rate, marking months of declining returns on such savings.

At the same time, the inflation rate (as measured by consumer prices) rose to 5 per cent. In effect, savers are getting next to nothing on such deposits due to rising inflation.

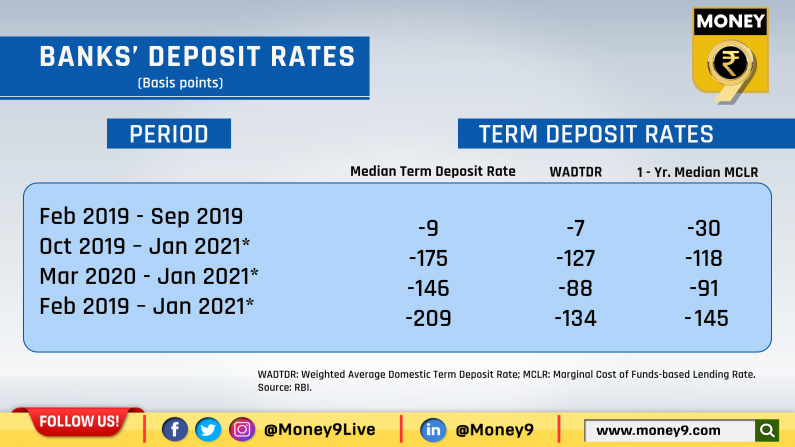

It is important to take a look at the median term deposit rate (MTDR), which had started to fall two years ago in February 2019.

The decline in the MTDR accelerated last March when Covid-19 pandemic hit the economy.

A month ago, the Reserve Bank of India (RBI) pointed out that the MTDR has moderated by 146 basis points (bps) from March 2020 up to January this year.

During the same period, the one-year median marginal cost of funds-based lending rate (MCLR) of commercial banks declined by 91 bps. The reduction in the cost of funds augurs well for transmission to lending rates. On the flip side, expectations are that the current deposit rates and conditions will continue in 2021-22.

In a report earlier this month, JM Financial pointed out that after witnessing a dip from July onwards last year, deposits growth had accelerated by December.

“Deposit growth is near the levels seen during the post-demonetization period. This, we believe, could deter banks from raising deposit rates sharply unless credit offtake improves materially over the next six to nine months and given that the incremental credit-deposit (CD) ratio remains at 40-42 per cent levels”, the report said.

A reason for the higher deposit growth is risk-aversion due to the uncertainty over job prospects and the overall economic situation.

Consequently, it is clear that any changes to this scenario can be expected only with an increase in credit offtake and a shift in the RBI’s current accommodative monetary policy stance.

At its last review of monetary policy in February, the committee held the repo rate at 4 per cent. The next policy review is scheduled for April 5-7 and comes at a time of higher inflation prospects due to elevated domestic fuel prices which provide an upward push to inflation.

For Indian savers, term deposits provide little (even without taking into account taxation) and the trajectory of rates seems to suggest that they will barely provide a meaningful return unless inflation cools down significantly and growth returns in an orderly fashion.

(The writer is a senior journalist and public policy commentator. Views expressed are personal. His Twitter handle is @szarabi)