FDs are evergreen! These 9 banks offer high interest rates

The interest rates on FDs have reduced by a wide margin. The rates are hovering around just about 5% in public sector banks.

In an era of ‘Robinhood’ traders when everyone is attracted to stocks and cryptocurrencies, the good old fixed deposits (FDs) are getting less attention. This is why it is all the more important to focus on it. When you create an investment portfolio, you should allocate some part of it to fixed deposits for the security and guaranteed returns it offers you.

FDs to never lose sheen

FDs make sense for people who want guaranteed regular income. For example, senior citizens can invest their savings in FDs to earn interest income. Similarly, a know-nothing investor who just received a huge amount of lumpsum money may consider putting it in a fixed deposit to earn regular income. Consider this – A home-maker wife has just lost her husband. She receives insurance money. She needs to take care of household expenses and school fee of her children. Should she invest this amount in the stock market? Certainly not! For her, the simplest thing to do will be putting this money in FDs to earn monthly interest income that takes care of monthly expenses.

Interest rates on FDs

The interest rates on FDs have reduced by a wide margin. The rates are hovering around just about 5% in public sector banks. These are about 100 basis points (or 1%) higher in some of private sector banks.

We have compiled a list of nine public sector banks that are offering best rates on normal FDs below Rs 1 crore:

Union Bank (5.4%), Punjab & Sind Bank (5.3%), State Bank of India (5.3%), Canara Bank (5.25%) and Indian Bank (5.25%) are the top five public sector banks offering highest interest rates on two-three years FD. The higher the tenure, the higher will be the interest rates.

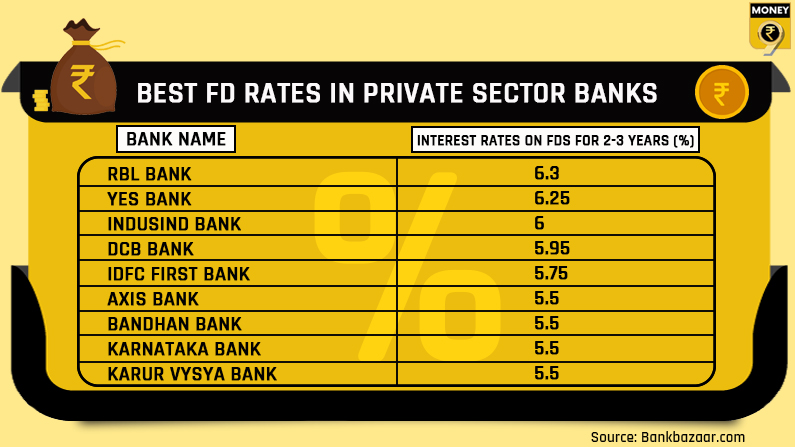

If you want higher interest rates, you may go for private sector banks that are offering attractive rates on normal FDs below Rs 1 crore. RBL Bank (6.3%), YES Bank (6.25%), IndusInd Bank (6%), DCB Bank (5.95%) , and IDFC First Bank (5.75%) are among private banks offering the highest rates on FDs.

Your money is safest with public sector banks. However, you may diversify your FDs in private sector banks too that will give you better rates. Remember each depositor in a bank is insured up to a maximum of Rs 5 lakh for both principal and the interest amount. This combines all deposits in a bank from savings, recurring to fixed deposits. It means that in case the bank goes bust in which you have your savings account or an FD is running, the Deposit Insurance and Credit Guarantee Corporation (DICGC), a wholly-owned subsidiary of the Reserve Bank of India (RBI), is liable to pay you up to Rs 5 lakh.

Fixed deposits are your friends in the investment world in thick and thin. Gift it their deserved place in your investment portfolio.