Five things to know about buy now pay later

Buy Now Pay Later is a one-click credit facility offered by many lenders and available as a payment option with select merchants

Buy Now Pay Later (BNPL) is a financing option that is fast gaining currency in the country. BNPL is a short-term no- or low-interest loan option that allows you to make purchases and pay them later. BNPL is often confused with a credit card. This is because like credit cards, BNPL also offers short-term loans, gives interest-free credit periods and sometimes also provides the option of converting your purchases into equated monthly instalments (EMIs). But the products also differ in many aspects. Let us understand five crucial things about this latest popular financing option.

What is BNPL?

Buy Now Pay Later is a one-click credit facility offered by many lenders and available as a payment option with select merchants. It is a small credit available easily that makes your shopping experience convenient. You are expected to pay off your dues in their entirety within a month to let your services continue.

How Does Buy Now Pay Later (BNPL) Work?

The BNPL settles your expenses on your behalf, and you need to repay your dues in the interest-free window. BNPL services generally offer a credit period that ranges from 14-90 days. However, this is based on your transaction value. The amount you get as credit is based on the lender. You just need to connect with your chosen BNPL provider through their website or app, complete the formalities of filling out forms and the KYC process to initiate the facility.

• Step 1: Sign up with your preferred BNPL service once you read the terms and conditions (T&Cs).

• Step 2: Add the desired items to the cart.

• Step 3: At checkout, choose the BNPL facility.

• Step 4: If you are approved for the service (you will be notified within a few seconds), you need to make a small down payment. This amount is generally 25% of your purchase amount (it can vary from one merchant to another).

• Step 5: You can pay off the remaining amount in instalments.

• Step 6: You can repay the balance amount via bank transfer. You can also opt for the amount to be deducted from your debit/credit card or bank account automatically.

Pros and Cons of Buy Now Pay Later (BNPL)

Pros

Convenience: The Buy Now Pay Later (BNPL) service is integrated with the merchant’s online store and you can opt for it at checkout. The transaction process is easy and it allows you to buy items and pay for them at a later date.

Easy To Set up And Instant Approval: BNPL providers do not look into your credit history before approval. You can easily sign up with any BNPL provider by providing your phone number, entering the verification code and setting up your bank account.

Interest-free: Interest is generally not charged on the amount that you borrow. However, a few BNPL companies may charge up to a 24% interest rate. This depends on the tenure, merchant, and borrower.

You Can Spread Out Your Payments: Instead of having to pay the entire amount in one go, you can repay the amount over a period of time, subject to terms and conditions. For example, you can repay in monthly or fortnightly instalments.

It is also important to note that timely repayments can reward you with either replenishing the credit limit or increasing the credit limit of the user at the beginning of the next repayment cycle. Some BNPL providers may also offer additional discounts or cashback for availing of their facilities as an incentive.

Cons of Buy Now Pay Later (BNPL)

Increases Spending Impulse: BNPL allows you to make a purchase of any amount and you can pay for it later. This can always be tempting. You can be encouraged to spend more than you can afford.

Attracts Late Payment Fees: If you do not repay the remaining amount on time, you will have to pay a late payment fee. If you do not have sufficient funds, you will be charged a late fee until you have the funds to make the payment.

Damaged Credit Score: If you miss payments, it will be reported to credit bureaus, and in turn, reduce your credit score. This will reduce your chance of getting a credit card or loan in the future.

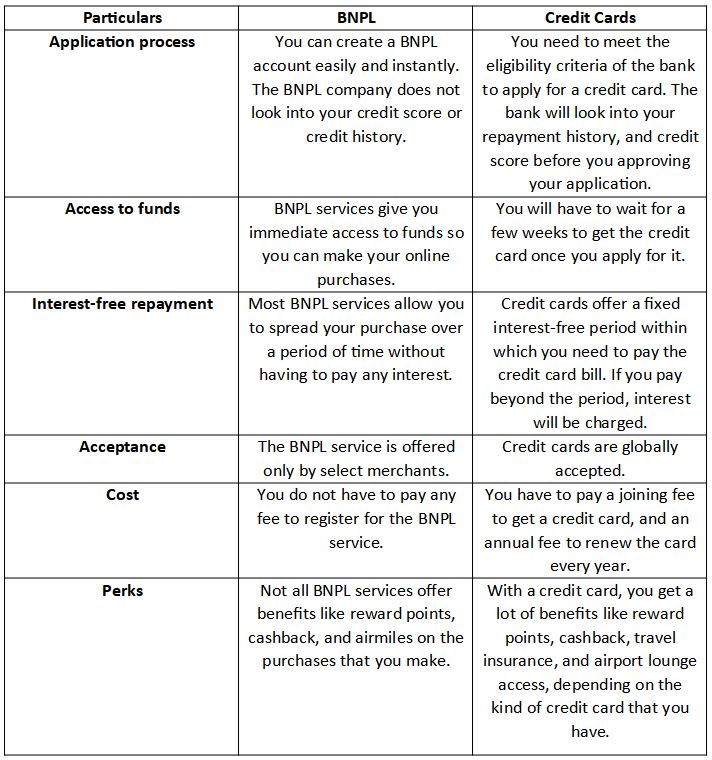

Difference Between Buy Now Pay Later (BNPL) and Credit Cards

Opting For Buy Now Pay Later (BNPL)

BNPL is one of the simplest way to avail credit to conveniently manage your expenses. However, do remember that it is a loan that needs to be ultimately repaid. You should consider opting for BNPL when you are not eligible for a credit card because of low credit score. BNPL offers you interest-free instant funds without look into your credit history. Also, BNPL providers allow you to purchase items and spread the cost over installments. Hence, it eases your financial burden and you can still buy what you want.

(The writer is CEO, BankBazaar.com; views expressed are personal)