Home loan from NBFCs: Lowest rates starting at 6.66%; check out 9 best offers

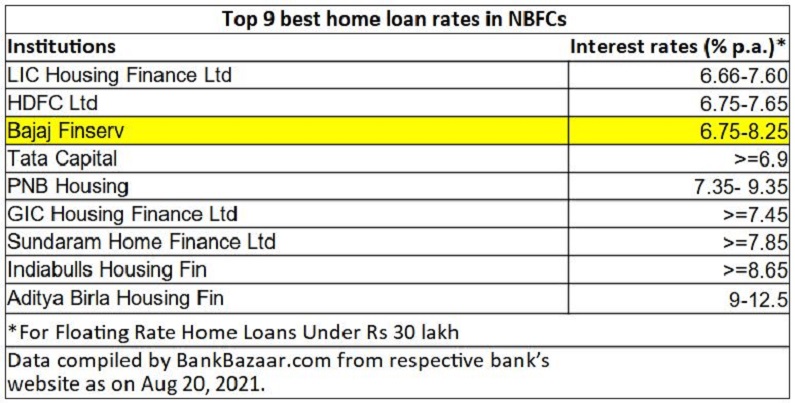

LIC Housing Finance, HDFC and Bajaj Finserv are offering home loan at interest rate in the range of 6.66% to 8.25%

Even as home loan rates in banks are cheaper, there could be some people who are not eligible for taking a loan from banks due to lower credit score or other reasons. If your bank has rejected your loan application, you may consider approaching non-banking finance companies (NBFCs) where credit assessment norms are relatively relaxed and the process is faster, although interest rates will be on the higher side compared to banks.

LIC Housing Finance, HDFC and Bajaj Finserv are offering home loan at interest rate in the range of 6.66% to 8.25%.

“NBFCs typically operate with higher cost of funds. This means that they have to lend at higher rates to offset the higher cost of funds. The higher pricing means that they have to take more risks compared to banks. So, they may lend to people with lower credit scores and approve loan applications even for properties where the title may not be absolutely clear or riskier classes of collateral such as land and panchayat property are involved,” says V Swaminathan, CEO, Andromeda and Apnapaisa.

We have compiled a list of 9 NBFCs offering best rates on home loans:

Benefits of taking home loan from NBFCs

If you don’t meet the loan eligibility criteria of various banks, the NBFCs will save the day for you, at a higher price. Apart from relaxed approach at creditworthiness, they are much faster at loan disbursal.

“When it comes to documentation, NBFCs have simpler and more flexible criteria. The loan processing time with NBFCs is also swifter than banks. So, if you are not eligible to get a home loan from a bank, then approaching an NBFC for a home loan can be a good idea,” says Adhil Shetty, CEO, BankBazaar.com.

One may get better valuation of properties that helps in fetching the higher loan amount. “NBFCs have more relaxed norms when it comes to loan-to-value ratio. While they cannot cover the complete cost, they can help a borrower get a higher loan amount by including additional costs related to homeownership, such as stamp duty charges, registration charges, etc., while calculating the loan-to-value ratio. This helps the borrower get a higher loan amount against the same property,” says Shetty.

Swaminathan says NBFCs also cover locations that the network of bank branches may not cover such as far-flung and remote areas.