Things to remember while refinancing your home loan

Refinancing home loans helps in increasing savings with lower interest payments, smaller EMIs, and shorter loan tenures

Home loans rates have been at historic lows. We have been seeing a continuing dip from 2019 when the lowest rates were around 8.40%. It is no brainer that the falling rates present homeowners with the opportunity to transfer their loans at lower rates. Refinancing helps in increasing savings especially during the Covid period with lower interest payments, smaller EMIs, and shorter loan tenures.

What is home loan refinancing?

Home refinancing involves paying off your existing home loan by taking off a new home loan with better terms such as a lower rate of interest. The new loan can be taken either with the same lender or a new lender.

In a paper presented by BankBazaar, it is explained that on a loan of Rs 50 lakh at 8.00% for 20 years interest works out to Rs 50.37 lakh. If this loan is refinanced at 7.00%, the interest falls to Rs 43.03 lakh, ensuring savings of nearly Rs 7 lakh, which can be used for savings, investments, and the achievement of various aspirations such as travel, vehicle upgrade, or higher education

Things to remember while refinancing your home loan

Lower Interest Rate

While transferring your loan make sure the difference between the old and new rates is at least 50 bps. Otherwise, it might not be very cost-efficient to go through the whole process of refinancing your loan. “Often the biggest part of homeownership cost is the interest on the home loan. A loan cheaper by around 50 basis points or more could lead to the shorter loan tenure, lower EMIs, lower interest payments, and large long-term savings,” stated in the BankBazaar report.

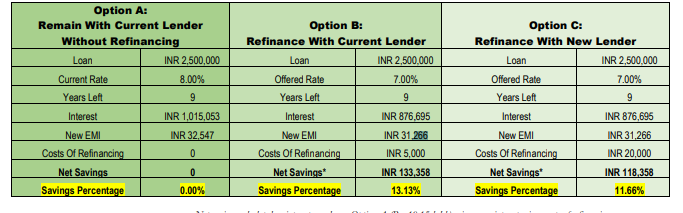

Processing fee

If your own lender is offering a rate lower than what you’re paying, then it is best to approach your lender and ask to be moved to the lower rate. This will attract the processing fee but when compared with the new bank this processing fee would be much lower since in case of a new loan more paperwork will be required.

Source: BankBazaar

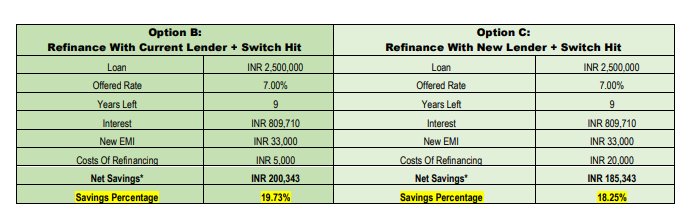

Don’t reduce your EMI amount

It is always advisable to not reduce your EMI amount as you can end up saving a lot more over the full tenure of the loan. The BankBazaar Switch Hit needs you to refinance and remain at your old EMI. This allows you to repay your loan faster, ensuring higher savings on interest. Continuing the above example, if the same EMI is continued then it can increase your savings substantially over the longer tenure.

Source: BankBazaar

Time left on your loan

Last but not the least, calculate the remaining tenure of your home loan. This is because you get the maximum benefit if the loan is refinanced during the early years. BankBazaar report states, “Refinancing early in your loan tenure –typically in the first half – makes more sense. During this time, your EMIs focus mostly on interest payments. Therefore, a refinanced loan at a lower interest rate will lead to savings.”