Top-9 banks with best interest rates on gold loans

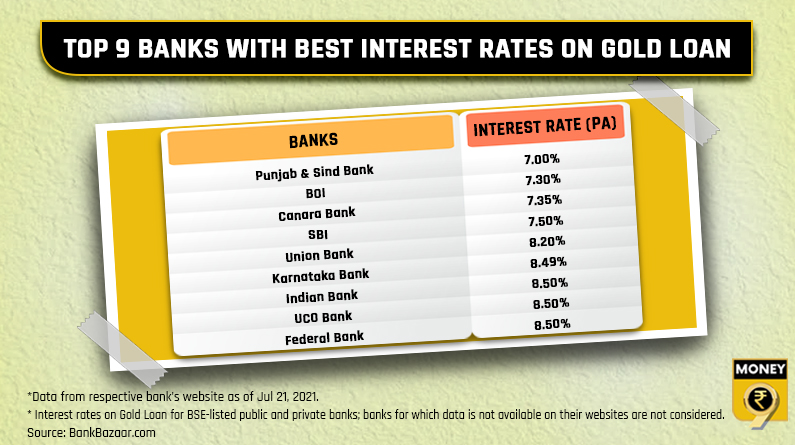

You may get gold loan for as low as 7% per annum from banks compared to a double-digit interest rate on personal loan in most cases

A secured loan is any day better than a personal loan given lower interest rates on the former. A secured loan is the one which is backed by a collateral. This could be your property, stocks, mutual funds and even insurance policies. What is most common, however, is loan against gold. While pledging gold jewellery for loan is seen in negative light, it can help you meet your short-term cash crunch at a cheaper interest rate.

You may get gold loan for as low as 7% per annum from banks compared to a double-digit interest rate on personal loan in most cases. Data from Bankbazaar.com shows Punjab & Sind Bank is offering gold loan at 7%, followed by Bank of India at 7.30% and Canara Bank at 7.35%. Among the top nine, Indian Bank, UCO Bank and Federal Bank are charging the highest interest rate at 8.50%.

How does gold loan work?

To borrow against gold, you need to pledge it with the bank. Gold jewellery is accepted for this purpose generally. As you produce your gold jewellery to the bank, it evaluates its purity and gets its valuation done. The purity has to be about 18-22 carat. It also checks your credit score before quoting the interest rate.

What is loan-to-value?

Remember you do not get loan worth the entire valuation of your gold. There will be a loan-to-value. It is a percentage figure on gold valuation. The Reserve Bank of India (RBI) has fixed an upper cap of 75% on the same for banks and non-banking finance companies (NBFCs). It was increased for banks to 90% until March 31, 2021, keeping in view the Covid-19 emergency.

Let’s understand LTV with an example. If the valuation of your gold jewellery is worth Rs 100, the bank will lend you up to Rs 75. This is done to keep a margin of safety in case gold prices fall from the current levels. If gold prices slump drastically, the bank may ask you to provide higher collateral.

“Even as the LTV limit is fixed at 75 per cent, most banks do not offer an LTV of more than 50 per cent unless your credit score is extremely good,” said Ankur Gupta, founder and CEO at Ruptok Fintech, a fintech platform for gold loans.

Gold loans are an efficient way to meet your short-term money needs. Understand all about LTV before you go for it. Know that a lower LTV is safer. Go for higher LTV only if you are sure about repayment and have additional collateral to produce in case of sudden crash in gold prices.