Savings funds now moving to FDs

Customers are increasingly shifting money from savings accounts to fixed deposits (FDs) as the interest rate differential between the two is widening.

People are now withdrawing their money from savings account and putting it in fixed deposits. The main reason for this is the huge difference between the interest rates available on savings and fixed deposits. The interest on savings account has remained stable for the last three years. While interest rates on fixed deposits have reached a record high. The interest differential between savings account and fixed deposit is currently at a record high of three years. There is currently a difference of 260 basis points between the interest rate available on savings account and fixed deposit account. This difference was 220 basis points in FY 2021-22 and 230 basis points in FY 2020-21.

Interest on FD is attractive

Banks are continuously increasing the interest rates on fixed deposit schemes to attract customers. Many major banks are offering up to 6.80% interest on FDs. On the other hand, only 2.7 to 3 percent interest rate is available on the savings account. Due to the high difference between the two, the interest of customers has increased in FD.

Depositing less money in savings account

Customers are increasingly shifting money from savings accounts to fixed deposits (FDs) as the interest rate differential between the two is widening. Where the highest interest is being received in FD at this time, the interest rate available in savings account has remained largely unchanged for the last three years. For example, the country’s largest bank State Bank of India (SBI) is offering 2.7-3 per cent on savings deposits, while 6.8 per cent on FDs of less than one to two years.

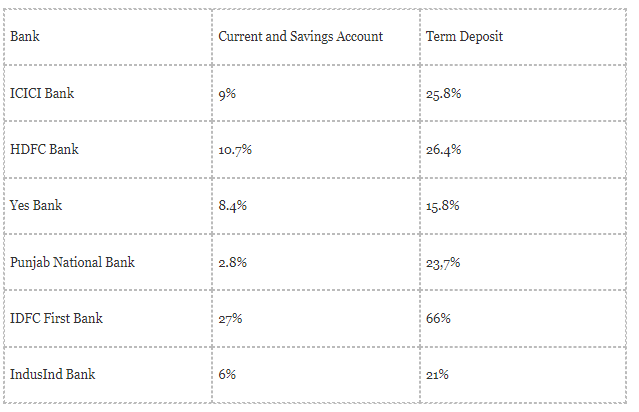

Increased term deposits in banks

An ICICI Bank official says that earlier the difference between savings and deposit rates was very less. As interest rates have increased, customers are now naturally turning to term deposits. He also told that till a year ago, ICICI Bank’s term deposit growth was 25.8%, while the current and savings account growth was only 9%. Customers are on the lookout for schemes with higher interest rates from the very beginning. According to RBI data, the rate differential between savings and term deposits is at a three-year high of 260 basis points. In the year 2021, this difference was of 230 basis points, whereas in the year 2022, the difference was of 220 bps.

YOY growth in Q1 FY24