Corporate FDs offer 1-3% higher return than bank deposits. Should you invest?

Company deposits offer an advantage over bank deposits by 1-3%

Low interest rates on bank deposits are now a major concern for citizens. They are looking for other fixed income options where they can invest their money. This is the reason financial planners say queries about corporate deposits have also shot up recently.

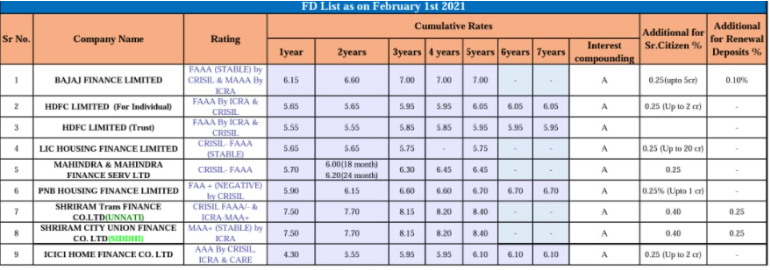

Corporate deposits are similar to banks FDs. These deposits are offered by companies and carry slightly higher interest rates. For example: currently, State Bank of India (SBI) is offering 5.40% interest on its five-year fixed deposit whereas company deposits are offering a return of around 5.5 to 8.40% for the same period. Consider this: Bajaj Finance Limited is having an interest of 7% per annum over a period of 5 years for the amount upto Rs 5 crore. Similarly, Shriram Trans Finance offers retail investors an annual interest of 8.40% over a period of 5 years.

The above examples show how company deposits offer the advantage over bank deposits by 1-3% depending upon the tenure. But before you get swayed by high interest rates you need to understand the risks involved in corporate FDs. Here is a primer on what corporate FDs entail:

What are Corporate Deposits?

Corporate FDs are similar to bank FDs. Bank FDs are offered by banks whereas corporate FDs are offered by companies. It is one of the ways by which companies, mostly NBFCs, raise money from the market to meet their business needs. In return, companies offer interest rate on deposits at a prescribed interest rate for different tenures ranging from 1 to 7 years.

“Corporate deposits give higher return than bank deposits. They also offer additional interest rate on renewal of deposits and senior citizens get an additional 0.25-0.40 % across all tenures. Moreover, there is an insurance guarantee up to Rs 5 lakh on bank FDs, which insures the savings of the person if a bank fails. There is no insurance with corporate FDs,” said Anil Chopra, Group Director – Financial Wellbeing, Bajaj Capital.

High Return

One of the benefits of corporate FDs is that they provide higher interest rates than bank FDs. Considering the risks involved in the business they pay higher interest rate to attract investors.

“The investor should understand that they give higher returns only because they are risky. Investors should invest in AAA-rated corporate FDs only. Do not look for lower-rated FDs to get higher returns,” said Kalpesh Ashar, a certified financial planner.

Source: Bajaj Capital

Risks Involved

Always remember that money deposited is at risk if the company defaults. In the past, we have seen instances when the company defaulted despite good credit ratings. For example: When Dewan Housing Finance Corporation (DHFL) launched its non-convertible debentures (NCDs) in 2016, it was subscribed over 6 times on the first day itself. The beleaguered housing finance company, however, defaulted on bond repayments in 2019. Similarly from the highest rating of AAA, IL&FS rating was downgraded in two months. The crisis surfaced in 2018 when the company defaulted on commercial papers, including debentures and term loans.

Taxability

Interest earned from deposits is taxable as ‘Income from Other Sources’ and are taxed according to your slab rate. It means if the gross income is within 10% tax bracket, then you will have to pay a tax of 10% on interest received. If the tax slab rate is 30% then the higher tax rate needs to be payable.

What to do?

Corporate FDs are riskier than conventional FDs as the deposits are unsecured.

“Investment in one corporate FDs should not be more than 5-10%. Given the risk involved, we only recommend FDs with AAA rating,” said Chopra.

“Corporate FD rates can be higher from bank FD rates by 1-3% depending upon the tenure. But given the risks involved I don’t recommend corporate FDs,” said Mrin Agarwal, founder, FinSafe India.