Fixed deposits: Top-5 banks giving higher interest rates

The interest earned on a FD is fully taxable. It is considered a part of total income and taxed as per the applicable tax slabs

A fixed deposit (FD) is one of the safest investment options which offers a fixed return. It is still a choice of investment for many middle-class Indians as it has negligible market-related risks and offers higher interest rates than a savings account. In an FD, the account holder can deposit a specific amount for a fixed tenure.

The bank offers interests, depending on the FD tenure and the deposit amount. This interest varies from bank to bank.

Term deposits are one of the conventional ways to invest money. One does not need to open a separate account for an FD. The amount in FD after attaining the maturity period gets deposited in

the bank’s savings account.

Interest earned from term deposit rates are taxable

The interest earned on a FD is fully taxable. It is considered a part of total income and taxed as per the applicable tax slabs. It falls under the category ‘Income from Other Sources’ in the Income Tax Return.

The banks levy TDS (Tax Deducted at Source) on the interest income from FDs. This deduction happens at the end of every financial year. Many people tend to have this misconception that banks deduct tax at the time a fixed deposit scheme matures and the interest earned is credited. But that is not the case.

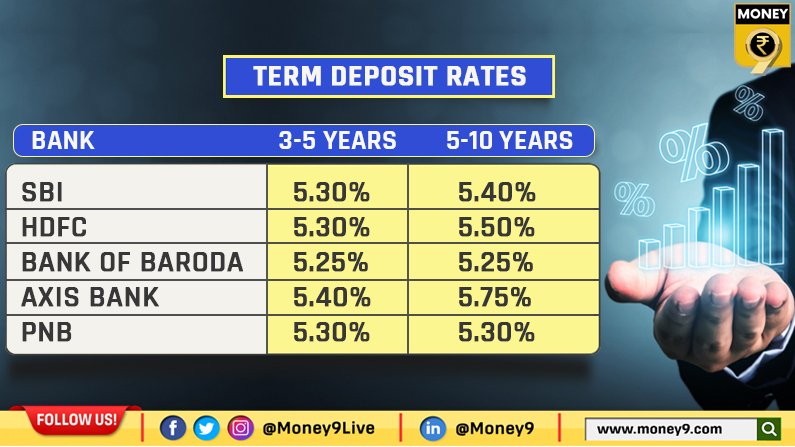

Before opening a fixed deposit in a bank, it is important to compare the latest fixed deposit rates among leading banks in the country.

Here are the latest fixed deposit rates:

(These interest rates are for domestic term deposits of less than Rs 2 crore for Indian citizens)