Facing a short-term cash crunch? Your Mutual Fund units can help

While you need not liquidate your mutual fund units to get this loan, you pledge some units with the lender. And then, you are charged interest only on the amount you utilize.

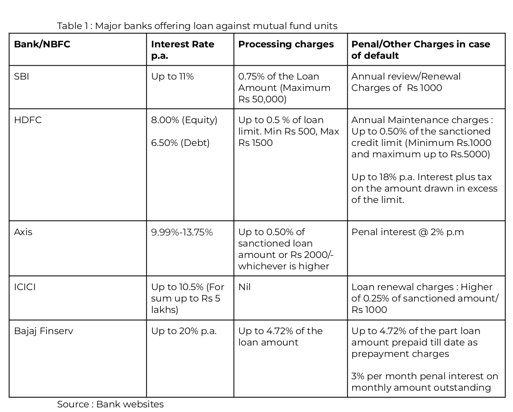

Loans against mutual funds units for wading through a short-term financial crunch are quickly catching the fancy of people. Even though they are easy to obtain and bide well for that month-end fund necessity or even medical emergency, there are a few things you should keep in mind.

While you need not liquidate your mutual fund units to get this loan, you pledge some units with the lender. And then, you are charged interest only on the amount you utilize. So, if you have a sanction limit of Rs 3,00,000, and you withdraw only Rs 1,50,000, you will end up paying the applicable interest only on this Rs 1,50,000.

Naturally, the interest charged is lower, since the loan is secured with your MF units, as opposed to unsecured personal loan, which has no collateral, and thus, is riskier for the lender.

Notes Agra-based financial planner Shifali Satsangee, “Such loans come by fulfilling instant/ current monetary requirements without redeeming the present mutual fund holdings, and therefore, without compromising on your long term goals”.

How much loan can you get?

Most banks offer up to 50% of the NAV (net asset value) of your equity mutual funds as maximum loan. This is because equity, being a volatile asset, is subject to greater market fluctuations. On the other hand, up to 70-80% of the NAV of your debt funds are available to you as the maximum loan amount. Even if you are a first time borrower, you can avail this loan.

Remember, while you will continue to earn dividends or interest on the units you have pledged with the lender, you won’t be able to sell them at your wish. Only once you’ve paid off the entire loan, will the lender let go of the lien on your units. In case you default or are unable to pay the loan, the lender will redeem these units, retaining the funds as payment towards their loan.

Generally, the tenure for such loans is 12 months, with the amount ranging from Rs 10,000-1,00,00,000. In some cases, like with SBI, the minimum loan amount has to be Rs 25,000. But in case the market dips, the lender will ask you to put in extra funds to compensate for their losses.

Says SEBI Registered Research Analyst and Certified Financial Planner Anupam Roongta, “The idea of this loan is to fulfill a short-term obligation. Taking a loan against MFs to invest further is not a good idea. If the market falls, you may have to pledge more or repay a certain amount. Be prepared for this. Also, understand the monthly interest payment cycle carefully. Otherwise, your CIBIL score could be adversely impacted”, he signs off