Stock at Stake: Can This Co Sail Through With India Growth Story?

In 2023, Demand in India is expected to increase at 7.3% (123MT) which is the 2nd highest after Turkey. Even in 2024 demand is expected to grow at 6.2% (131MT).

In the News

Steel Authority of India Limited (SAIL) is in the news after LIC has increased its ownership in the company from 6.93% to 8.67%. In morning trade on Monday (12th June 2023), SAIL went up 1.21%, it ended the session at Rs 83.60 with gain of 0.84%. Although LIC has increased its stake but is it a good company to invest in? Let’s find out by looking at its fundamentals.

External Sector

The performance of steel companies is largely driven by the external environment. Globally economy is expected to slow this years due to tighter financial conditions, geopolitical tensions and lower consumption because of inflation. Still, SAIL reported, citing WSA that 1885 Million tonnes (MT) was produced in 2022. India’s production grew by 5.8% and it was the only major country besides Iran to have positive growth in production. India is 2nd largest producer steel producer in the world. With Odisha, Chhattisgarh, Jharkhand and Karnataka having maximum steel production capacity.

Meanwhile, global steel consumption is expected to go up from 1782MT to 1822 and 1854 in 2023 and 2024 respectively. during 2023, Demand in India is expected to increase at 7.3% (123MT) which is the 2nd highest after Turkey. Even during 2024 demand is expected to grow at 6.2% (131MT).

Factors like high infrastructure spending by the government, PLI schemes, revival in Capex by Indian Inc., boom in hospitality and real estate sector bode well for steel demand. Still, if regulatory and bureaucratic issues in India will be further eased then it will lead to more FDI and higher steel demand.

Company’s Business

Steel Authority of India Limited is Public Sector Undertaking. It is a Maharatna CPSE. It is the country’s largest steel producer and the world’s 20th largest.

5 integrated plants

– Bhilai

– Durgapur

– Rourkela

– Bokaro

– Burnpur

3 special steel plants:

– Durgapur

– Salem

– Bhadravati

4 Subsidiaries:

– SAIL Refractory Company Limited (SRCL)

– SAIL Jagdishpur Power Plant Limited

– SAIL Sindri Projects Limited

– Chhattisgarh Mega Steel Limited

Mining:

– Iron Ore: 33.776 MT

– Limestone: 1.362 MT

– Dolomite: 0.451 MT

Production:

– Hot Metal: 19.409 MT

– Crude Steel: 18.291 MT

– Saleable Steel: 17.246 MT

Distribution:

– Network of around 4800 distributors

– Domestic Sales (97%)

– Exports (3%)

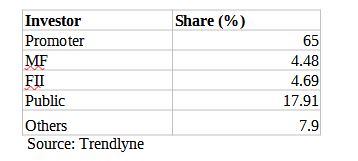

Shareholding Pattern (As on 31st March 2023)

Growth Drivers

1) Although the global outlook is dim, the domestic outlook for steel demand is better and that’s more relevant for the company as exports account only 3%

2) For FY24 Management gave sales guidance of 18.7 MT which is 15% higher than the previous year.

3) Huge capacity addition to aid growth over long term

Competitive Advantage

1) Plants are strategically located in mineral-rich areas

2) Focus on efficiency by debottlenecking (Focus on where inefficiencies in production can be improved) to increase the capacity of existing plants by 2.5 to 3 Million Tonnes

3) Plan on huge capex in the next 9-10 years and increase its steel production capacity to 35 million tonnes (MT)

4) Focus on improving employee skills and capabilities has increased labor productivity from 248 TCS (Tonne of crude steel) Man Year to 474 TCS Man Year.

5) Company reported that one of the highest expenditures on R&D led to the development of more than 100 products in recent years.

6) Company is also focusing on sustainability and environment protection which may help with reputation.

7) Small traders have been asking SAIL to change its distribution policy and make it easier for them to become distributors of SAIL. If this happens then the distribution market would become more competitive which would reduce the bargaining power of big distributors.

8) Company is focusing on digitization but they seem more around systems and ERP. Hardly any focus is there on Artificial Intelligence, Machine Learning.

Risk

– Volatile raw material prices

– Cyclicality in steel demand

– Besides digitization, a focus on advanced data analytics is required which seems to be missing.

– Differentiating the product in commodity business requires constant innovation and that is difficult for PSU which is loaded with tradition and that makes it resistant to change.

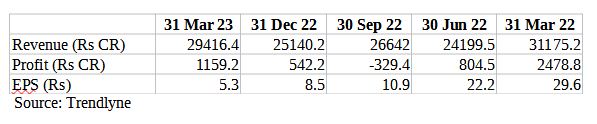

Financials (Consolidated)

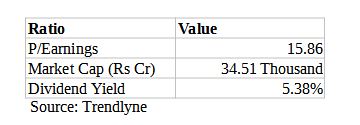

Valuation Ratios

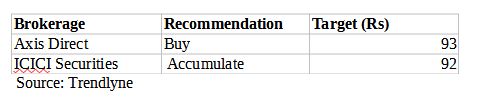

Brokerage Targets

So, company has growth potential strong competitive advantages and it’s CMP (Current Market Price) is 83.55, as per brokerage target there is around 10% upside potential in the stock.