Will Cyient DLM give you giant returns?

Money raised will be mostly used in working capital needs, debt repayment and small amount for capital expenditure as well as for inorganic growth.

Cyient DLM IPO is up for grabs and it has garnered some good responses from investors. It has been subscribed close to 8 times and it GMP is Rs 105/ share. So let’s have a look at the company.

IPO Details:

– Price Band Rs 250-265 / Share

– IPO will be open for subscription from 27 June – 30 June

– Company is looking to raise Rs 592 crore from IPO

– All of this Rs 592 crore will be fresh issue

– By the time of writing story IPO got subscribed 7.19 times

– GMP: Rs 105 /share

External Outlook:

Company is in the business of electronic manufacturing services. It is a leading integrated company in the space that is poised to grow. Global electronic industry grew by 3.9% CAGR between CY2016-CY2021, from CY2021 – CY2026 it is estimated to grow at 4.9%.

India has also taken various initiatives to promote the industry such as PLI, Merchandise Export Scheme. Also, global strategy of China+1 presents the case for growth. At the same time, India has resolved trade disputes with US so that will also help with growth and better relations. Due to all this, the company reported that the electronics industry in India is expected to grow at CAGR of 18.4% between FY22-FY27.

Company Profile:

Cyient DLM was established in June 93. It is a subsidiary multinational company Cyient. Cyient DLM provides Build-to-Print (B2P) and Build-to-Specification (B2S) services to sectors like Aero, Defence, Medical among others. It has key clients like ABB, BEL, Thales etc.

It is involved in design & development, build and also in maintenance. The company also provide services such as turnkey solution, series production, IoT Platform Implementation.

The company has 3 plants in Mysuru, Hyderabad and Bengaluru.

Purpose of IPO:

Money raised will be majorly used in working capital needs, debt repayment and small amount for capital expenditure as well as for inorganic growth.

Company’s competitive advantage:

1) Company has a diverse product portfolio and capability across the value chain.

2) It has the support of the parent company that helps with technical know-how, management expertise.

3) Company also has long experience in and technical expertise in complex industries such as aero, defence, medical etc.

4) It has long-term relations with clients. Coupling this with the above point creates high entry barriers

5) Company has a huge order book of above 2400 crore which provides revenue visibility.

Company’s risk:

1) Company’s order book is concentrated as the top 10 customers account for 91% share. This may reduce bargaining power.

2) They have a very low market share of just 0.5% in Indian EMS as per the report of Frost&Sullivan

3) Their customer count has also fallen from 50 in FY22 to 35 in FY23.

4) Their business is concentrated in a few sectors such as 42% in defence, 11% in Industrial, 15% in Aerospace and 30% in Medical. So their future revenue is dependent in the growth outlook of these industries. It would help more if company can further diversify.

5) Although the company’s order book has increased its profit has fallen 20.27% in FY22 as compared to FY22.

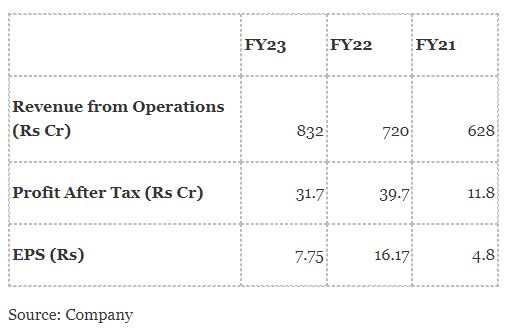

Financials:

Brokers Recommendation: