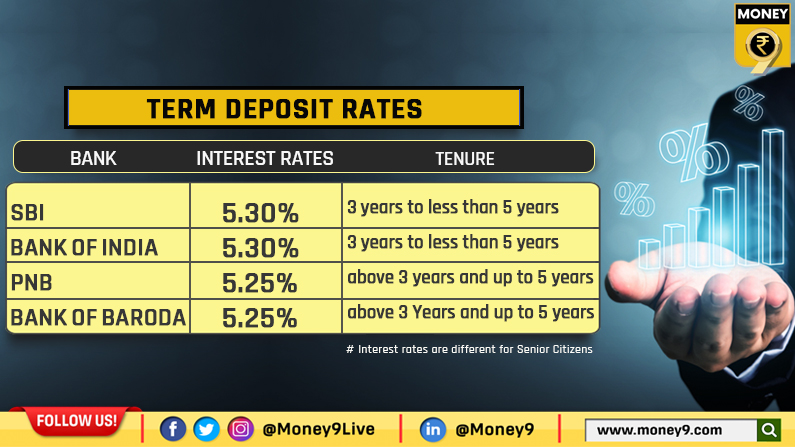

Fixed deposit rates of top four public sector banks

A fixed deposit (FD) is one of the safest investment options which offers a fixed return without any market-related risks

A Fixed Deposit (FD) offers better returns than a savings account and consolidates funds for a specified tenure at a fixed rate of interest, which can vary from 10 days to 10 years.

This is why FD is still one of the popular investment options in the rural as well as the urban market.

FD is one of the safest investment options which offers a fixed return without any market-related risks.

The bank offers interests, depending on the FD tenure and the deposit amount. This interest varies from bank to bank.

Many public sector banks offer FDs with good returns. Public Sector Bank (PSBs) is a type of bank, where a majority stake (i.e. more than 50%) is held by the government.

The interest earned on an FD is fully taxable. It is considered a part of total income and taxed as per the applicable tax slabs. It falls under the category ‘Income from Other Sources in the Income Tax Return.

The bank levy TDS (Tax Deducted at Source) on the interest income from FDs. This deduction happens at the end of every financial year.

The Reserve Bank of India’s repo rate and the reverse rate is at 4% and 3.35%, respectively, as per its monetary policy. The Reserve Bank of India uses the repo rate as a control mechanism to increase or decrease liquidity in the economy. Any change in repo rate impacts the cost of credit for commercial banks. This eventually impacts the retail lending policies of commercial banks by bringing change in home loan interest rate, rates on bank deposit, etc.

Here are the latest fixed deposit rates:

(These interest rates are for domestic term deposits of less than Rs 2 crore for Indian citizens)