Home loan prepayment: When is the right time to opt for it?

A borrower should always check the number of remaining years and opportunity cost before prepaying home loan

Do you have extra cash and are looking to prepay your loan? While pre-payment can help you close the loan early, investing in high return avenues can help you save for future goals. Given the dilemma, experts said one has to look at various factors while deciding between the two.

For example, an individual needs to analyse the opportunity cost while deciding whether to prepay or invest. The individual also needs to check the number of remaining years, as prepaying at the beginning of the tenure can reap you more benefits than prepaying towards the end.

“It is always better to pre-pay early on during the loan tenure. A prepayment made in the first five years of the loan will have a bigger impact than if it is made later in the tenor. This is because interest will still be a major component of your EMI in the earlier years, and prepayment would be mean higher savings,” said Adhil Shetty, CEO of BankBazaar.com.

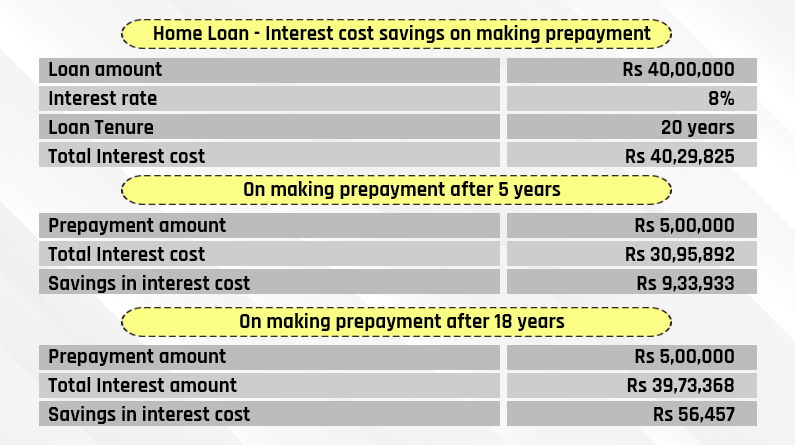

For example, consider a loan of Rs 40 lakh at 8% interest and a loan tenure of 20 years. The total interest payable on the loan is Rs 40.29 lakh. If you pre-pay Rs5 lakh in the fifth year of the loan, the total interest payable comes down to Rs 30.95 lakh, which means savings of around Rs 10 lakh. However, if you pre-pay Rs5 lakh in the 18th year instead, your total interest payable comes down only by Rs 56,457.

Source: Paisabazaar

Should you prepay in the falling interest rate market?

Pre-payment helps in closing your loan much earlier, as it saves on additional interest. But should one wait to prepay the home loan in the falling interest rate market, especially when you can earn a higher return?

A borrower needs to keep two things in mind while making pre-payments, according to Shetty.

“If your prepayment isn’t going to save you a lot of interest, such as when you make the pre-payment later in the tenor of the loan, then you may want to consider the opportunity cost of making a pre-payment vs. putting the funds in an investment that provided higher returns,” he said.

Experts feel borrowers should also look at the opportunity cost of investing your money.

“Purely from a financial perspective, a loan should be prepaid when you feel the money can earn less for you than the rate of interest on the loan. This is because if you feel that you can make 10% by deploying your money in a mutual fund, you make much more by doing so than by saving 6.7% on a home loan,” said V Swaminathan, CEO Andromeda & Apnapaisa, a loan distributor company.

Cost Involved

There are no pre-payment charges associated with floating rate home loans. There may, however, be different conditions attached to the prepayment. For instance, there may be a limit on the number of times you can make pre-payments in a year. While making prepayment also take into account the tax benefits you have from the home loan. Moreover, check the terms and condition of prepayment for cutting out last minute surprises.

What to do?

Those planning to avail of home loans in the near future can consider its variant known as home loan overdraft or home loan interest saver. Under this option, an overdraft account is opened in the form of savings or a current account, which is then linked to the home loan account.

“The home loan borrower can deposit his surpluses in the overdraft account and can withdraw from it to meet their fund requirement. The interest component of the loan account is calculated after deducting the monthly average balance of the overdraft account from the outstanding loan amount. This results in interest cost savings for the home loan borrower without impacting liquidity,” said Ratan Chaudhary – Head of Home Loans, Paisabazaar.com.