Will home loan rates surge in 2021? Here's what experts say

Experts say that the increasing inflation due to disruption of supply chains during the lockdown also has an impact on the interest rates.

Until March 31st this year, home loan rates were at their lowest which triggered a housing demand even during the pandemic. Since then, there have been indications that home loan rates are likely to go up. In April, the State Bank of India increased home loan rates by 25 basis points to 6.95%. However, in May, the bank again reduced the home loan rates to 6.70%. Will other banks follow the country’s largest lender? Are these low rates sustainable or have already bottomed out?

Ratan Chaudhary – Head of Home Loans, Paisabazaar.com says, “Other lenders too might follow SBI by reducing their lending rates, maybe with a time lag, for incentivising new home loan applications. However, it would be difficult to predict how long this trend will continue as there has been no change in the repo rate.

Experts say that the increasing inflation due to disruption of supply chains during the lockdown also has an impact on the interest rates. While we may not see any changes immediately, there are strong indications that interest rates will harden over the year.

Adhil Shetty, CEO, BankBazaar, says, “While rates will continue to hold steady in the near future, borrowers should be prepared to see rates go up especially in the second half of the financial year.” He further adds that the second wave of Covid-19 has upset the applecart. The government has already been pressed into borrowing to support relief measures undertaken last year.”

Shetty added, “ The extension of these relief measures due to the loss of life from the second pandemic, the lockdowns, and the ensuing financial hardships, coupled with the need for financing the vaccine drive means that government need to borrow more. This will eventually push rates up even if retail demand is relatively subdued.”

Will the RBI slash the rates more?

Home loan rates in India have already seen their lowest at the end of FY21 and even the real estate experts declared this time the best for buying houses. Also, the monetary policy committee kept the repo rates unchanged at 4%. But will the RBI slash the rates more?

RBI’s Monetary Policy Committee (MPC) sets the repo rate on the basis of multiple factors, chief among them being rate of inflation, credit growth rate, deposit growth rate, economic growth, bond yield curves, policy decisions taken by other major central banks, etc.

Shetty asserts, “Increased borrowing by the government as well as higher inflation due to the pandemic will lead to a revision in repo rates. However, this may take some months to develop and is not expected in the near future.”

Strategy for Existing borrowers

Existing home loan borrowers with sufficient surpluses can also prepay to reduce the risk of increased EMIs caused by a rising interest rate regime in the near future. Chaudhary tells, “They should also compare the home loan rates offered by other lenders on exercising home loan balance transfer (HLBT) option. If the home loan interest rate offered by other lenders is significantly lower and leads to substantial savings in interest cost after factoring in the costs associated with HLBT, then they should transfer their existing home loans to the lenders offering the lowest interest rates.”

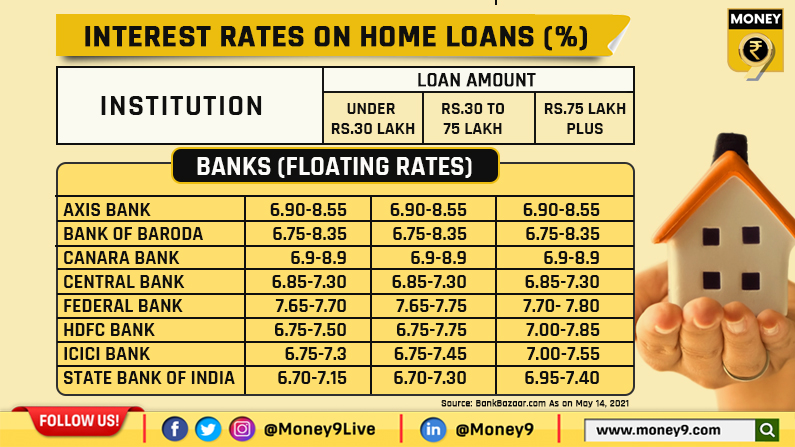

Here’s the table of interest rates on home loans by different banks:

Strategy for New borrowers

For new borrowers, the most important factor for securing an inexpensive loan continues to be a good credit score. “If you are considering investing in a house, make sure you have a good credit history and score as this will keep your loan rate low. Also, banks charge a spread over the external benchmark rate,” suggests Shetty.

The spread of the loan varies from bank to bank and often between schemes offered by the same bank. Select the lender with the lowest spread as the market forces and regulatory policies would bring the rates at par eventually, however, the spread would remain constant for the term of the loan unless specified otherwise in the loan documents, he adds.