HDFC Life Sanchay Plus: Should you invest?

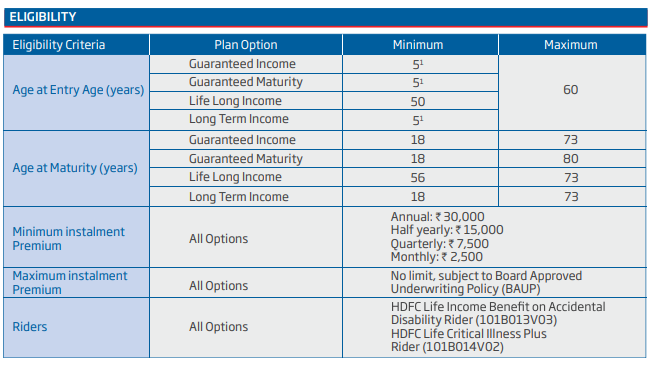

HDFC Life Sanchay Plus: The minimum age for buying the policy is five years and the maximum age is 60 years.

HDFC Life Sanchay Plus is a non-participating traditional life insurance plan, which offers a risk cover along with an investment component. It gives its policyholders a choice to earn guaranteed payouts after the completion of the policy term. One can invest in the policy by paying premiums annually, half-yearly, quarterly or monthly. A policyholder can also choose to receive regular benefits at these frequencies.

Features

The minimum age for buying the policy is five years and the maximum age is 60 years. Similarly, at the time of maturity, the eligible minimum age is 18 years and the maximum age starts from 73 years.

This policy requires a minimum premium instalment payment of Rs 30,000 a year with no upper limit.

Here are the four options that the policy offers to choose from depending on your life stage and goals in life

1) Guaranteed maturity

This option pays a guaranteed amount on maturity as lumpsum at the end of the policy term provided all premiums are paid and the life assured survives the policy term. The policy is for a term of 10, 12 and 20 years with the Premium Paying Term (PPT) option of 5 years, 6 years or 10 years.

Here the maturity benefit equals the guaranteed sum assured on maturity plus guaranteed additions. The guaranteed sum assured is total annualised premiums paid during the premium paying term. Guaranteed additions (GA) accrue at every policy anniversary after the premium payment term for 5 and 6 years. For PPT of 10 years, GA starts to accrue from 8th policy year.

Payout: For example, if a 30-year old male invests Rs 1,00, 000 (excluding 4.5% GST on 1st year and 2.25% from the 2nd year onwards) for the period of 10 years, the person will receive Rs 22,06,300 the end of 20 years. The XIRR or net yield works out to 5.55%.

2) Guaranteed Income

This option pays a guaranteed income for fixed-term 0f 10-12 years upon payment of all premiums. The policy term options are 11 and 13 years for PPT of 10 and 12 years.

Maturity benefit as a guaranteed income will be paid from 12th year to 21st year for the policy with a term of 11 years and PPT of 10 years. Similarly, guaranteed income will be paid from 14th year to 25th year for the policy term of 13 years with a PPT of 12 years.

Payout: For example, if a 30-year old male invests Rs 1,00, 000 for 10 years (excluding 4.5% GST rate on 1st year and 2.25% from the 2nd year onwards), the person will receive Rs 1.88 lakh for the period of the next 10 years. The XIRR works out to 5.9%.

3) Long Term Income

This option offers a guaranteed income for a fixed term of 25-30 years and the return of premium at the end of the payout period. The policy year can be 6,7,11 and 13 years for the premium paying term of 5,6, 10 and 12 years. For the PPT of 12 years guaranteed income will be paid from 14th year to 38th year in arrears.

Payout: For example, if a 30-year old male invests Rs 1,00, 000 (excluding 4.5% GST rate on 1st year and 2.25% from the 2nd year onwards) for the period of 12 years, the person will receive Rs 1,29,750 from the 14th year onwards for 25 years lakh for the period of next 10 years. The XIRR works out to 6.4%.

4) Life Long Income

This option offers a benfit of guaranteed income up to the age of 99 years and a return of premium at the end of payout period. For the Lifelong Income option alone, the minimum age at which you can sign up is 50 years.

Death scenario

In case of death of the life assured, the sum assured is paid to the nominee. Sum assured on death is the highest of:

• 10 times the annualized premium, or

• 105% of total premiums paid, or

• Premiums paid accumulated at an interest of 5% p.a. compounded annually, or

• The guaranteed sum assured on maturity, or

• An absolute amount assured to be paid on death, which is equal to the sum assured.

If the policy holder dies during the payout period, the nominee will keep on getting this guaranteed benefit. On the demise of the nominee in the payout period, the legal heir will receive payout benefits.

What to do?

The product suits conservative investors who appreciate assured returns over a long period of time. Moreover, the guaranteed plan qualifies as an insurance scheme under the Income Tax Act because it offers insurance cover as well, which in turn allows cash flow to be tax-free. This lends them a huge edge over similarly structured deferred annuity plans where pension income is taxable. For investors in the higher tax bracket of 20% and 30% tax brackets, a 5-6% tax-free return can be a clinching deal in the current market.

On the downside, the income generated will not be inflation-adjusted and tax laws can change in future. If it happens the return will not be so attractive from the policy. You can consider diversifying by having equity or hybrid funds in your retirement portfolio.