Insurance cover for maternity expenses; here's what all is included and excluded

Maternity Insurance: The certainty of a claim being filed is absolute, hence, the insurers levy a higher premium on these policies.

Women certainly have different health coverage needs as compared to men. The first and foremost reason why women mostly walk into a hospital is maternity. Realising the need there are health insurance plans that cover maternity and related medical expenses. But not all insurers offer this cover as many consider it as a planned activity.

“In the books of insurance, maternity insurance is considered as a pre-existing condition that is a planned activity by the people. Hence, a limited number of insurance companies offer maternity insurance in their plans. Generally, people don’t depend on policies for maternity as it costs Rs 25,000- 40,000 approx which people pay from their pocket. However, considering the increasing cost of maternity via cesarean section has become expensive in metro cities,” said Naval Goel, Founder & CEO, PolicyX.com.

Who should buy a maternity cover?

Experts say a health insurance policy with maternity benefits for an unmarried daughter or for a newly married couple would be very beneficial given the waiting period attached. “We have heard of cases where newborn children were diagnosed with coronavirus or Black fungus. In such cases it becomes advisable to buy a maternity cover, especially young women who have just started their career and plan to marry a couple of years down the line,” said S. K Sethi, director and founder RIA Insurance Brokers.

Goel agrees. “People who are getting married or planning a family must consider the maternity cover to ensure that their maternity journey becomes smooth and financially burden-free. Also, there is a lesser-known fact about maternity insurance that it is available in female individual plans, not in male individual plans.”

What does maternity cover offer?

There are several plans available in the market which are designed to cover maternity as one of the prime benefits. These plans cover delivery expenses (both normal and cesarean), other medical expenses such as nursing, room charges, doctor consultation, anesthetist charges and surgeon fees. The policy also cover the medical expenses of a newborn generally up to 90 days from the date of birth. Moreover, the maternity benefit covers the treatment taken for complications in the pregnancy or medically necessary termination, in case required.

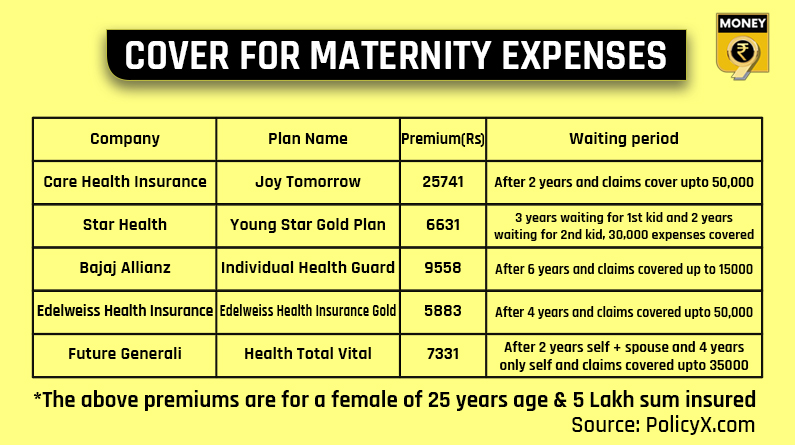

Waiting period

It is not that insurers have started offering maternity covers only now. These have in the market for years. While some have a waiting period of as long as 6 years others have reduced the waiting period to just 9 years. For example, Care Health Insurance offers a policy called Joy Today, where the waiting period is as less as nine months. Having said that, it is a three-year policy, which means you have to pay a premium for three years in one go.

Premium Paid

The premium payable on a maternity insurance policy is relatively higher than a regular health plan. “The certainty of a claim being filed under the policy is absolute, hence, the insurers levy a higher premium on these policies. Therefore, when one decides to buy such coverage, it is recommended to undertake a detailed cost-benefit analysis between different plans offered by various insurance providers. It is crucial to remember that as one grows older, the premium for maternity insurance increases. Furthermore, pregnancy-related costs are escalating every day,” said Goel.