Master the art of choosing a student travel insurance

As the world continues to battle the unprecedented impact of the Covid-19 pandemic on both domestic and international travel, students planning international studies need to take care of one major issue, a travel insurance. A student travel insurance provides coverage against medical expenses, luggage, and stay-related risks involved while travelling abroad for education. “An ideal […]

As the world continues to battle the unprecedented impact of the Covid-19 pandemic on both domestic and international travel, students planning international studies need to take care of one major issue, a travel insurance.

A student travel insurance provides coverage against medical expenses, luggage, and stay-related risks involved while travelling abroad for education.

“An ideal travel insurance covers medical expenses, non-medical expenses like study interruption, bail bond, personal liability, sponsor protection, loss of laptop, etc.,” Sourabh Chatterjee, President & Head – IT, Web Sales & Travel, Bajaj Allianz General Insurance told Money9.

Many people realized the importance of travel insurance after the Covid-19 pandemic peaked in an unprecedented fashion across the globe. Students were stuck in hostels or rented flats abroad while colleges were shut and lectures shifted online. A good travel insurance would have come in handy in such situations.

“Students should opt for an Indian travel insurance policy which provides adequate financial guard in an unknown foreign land and in unanticipated condition. They should focus on their studies and let student travel insurance ensure they do not face any difficulty while they are on their path to reach their dreams,” Chatterjee advised.

Several students faced last-minute flight cancellations, airport shutdowns, and even complete lockdown during the early weeks of March 2020.

“I was a final year student of computer science at the University of Wisconsin-Madison in the USA when the first wave of Covid-19 hit. There was complete lockdown even before I could hop onto a flight back home to India. I kept reminding myself that if a medical emergency occurs, I do have my travel insurance at hand,” Tarini Krishnan, an IT student in America said.

Students who travelled to the UK for their masters last year had a similar experience. They remained locked up for the entire semester due to health concerns amid rising cases of the virus in many parts of the country.

“I came to London last year in the midst of Covid-19 to pursue my masters. However, things became very difficult in the past few months with constant lockdowns and health concerns in a foreign land. I have an acute dental condition that requires regular monitoring. Dental treatment in London is quite expensive and I had opted for university insurance to cover these expenses. But things were so chaotic during my arrival, I couldn’t manage to get the documents from the university on time since we were quarantined and it caused me a lot of problems,” Nidhi Rawal, a business management student said.

For countries where travel insurance is considered an important admission document, most universities offer a medical insurance plan for international students.

“But many universities based in the USA typically pay for only medical expenses, cost of which is approximately $1,700 which is approximately Rs 1,25,000,” Chatterjee asserted. More often than not, premiums for these travel insurance plans are comparatively cheaper and easily accessible if bought domestically.

“The domestic premiums are lesser by nearly 1/3rd of the premiums payable for the policies offered by the universities abroad,” Policy Bazaar quoted on its website.

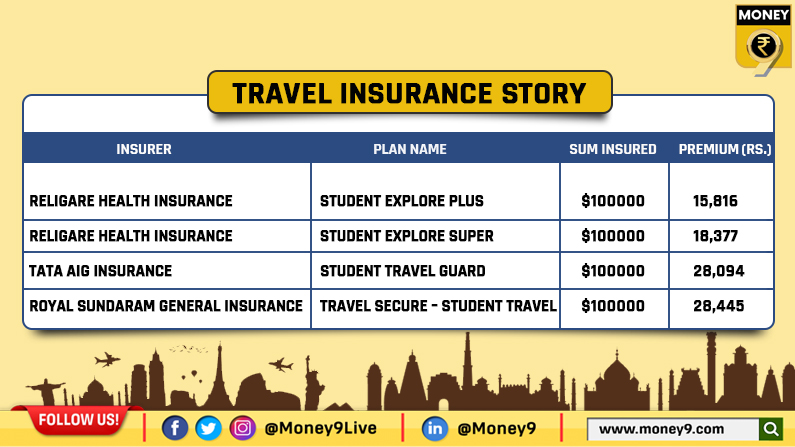

A price comparison of top domestic insurers offering travel insurance to a 20-year-old student travelling to the US for a 1-year university program. (Source: PolicyBazaar)

So, which is a better pick overall: Domestic travel insurance or University travel insurance?

“It is recommended to opt for an Indian insurance policy since every university-provided policy has a limitation of hospital network whereas Indian insurance policyholder is free to visit any hospital of the state and country. An Indian insurance policy covers the cost of bringing a relative to visit you following a medical emergency and your legal personal liability for damages if you accidentally injure someone, or damage their property,” Chatterjee explained.

Notably, the university insurance policy has co-pay option. For example, if the total bill comes to $3,000, a certain fixed percentage like 10% or 20% is to be borne by self if it is a non-network hospital or sometimes in a network hospital as well. It strictly covers only medical and accidental injury treatment.

Meanwhile, during vacations, if a student is traveling to a nearby country for leisure or a personal trip, the university insurance policy doesn’t cover this scope in most cases.

“However, an Indian insurance policy covers losses incurred due to loss of passport, loss of laptop, trip contingencies and baggage contingencies, etc.,” he said further.