Car insurance: Things you need to keep in mind for peace of mind, on and off the road

During a discussion, we stared calculating the cost of maintaining Honda car costing Rs 12 lakhs. I am not a Cost Accountant. But the calculation in a very simplistic manner turned out to be as follows: Reduction in market price of the car during first year (20% of Rs 12 lakh) = Rs 2.40 lakh […]

During a discussion, we stared calculating the cost of maintaining Honda car costing Rs 12 lakhs. I am not a Cost Accountant. But the calculation in a very simplistic manner turned out to be as follows:

Reduction in market price of the car during first year (20% of Rs 12 lakh) = Rs 2.40 lakh

Interest cost @9% of Rs 12 Lakhs = Rs 1.08 lakh

Driver salary @Rs 14,000 per month, may be higher = Rs 1.68 lakh

Petrol cost (assuming 8000 kms in a year @8 kms/liter ) = Rs 0.95 lakh

Servicing cost = Rs 0.20 lakh

Maintenance/batteries/tyres = Rs 0.30 lakh

Insurance cost = Rs. 0.40 lakh

Total = Rs. 7.01 lakh

If we divide this by 8,000 kms covered in a year, then the cost comes out to Rs 88 /km. No need to tell you what Ola or Uber costs because if you are living in tier-2 or tier-3 city. then owning a car has benefits of flexibility or say freedom . You will realise that whatever you invest in buying a car, more than half of its price is going out of your budget on a yearly basis .

Why do people buy, maintain and use cars? It is basically to show their status. They want to impress others by showing their status, achievements in the organisation, going to market, pilgrimage or for attending weddings .

It is surprising that after having invested Rs 12 lakh in car and incurring cost of Rs 7 lakh in a year, when it comes to buying insurance policy, then they get affected by L1 syndrome and start looking for cheapest, defeatured insurance product, which does not even meet expectations. This syndrome is a disease which affects large number of people in our country. Under its influence, the person is thinking of buying only the cheapest product.

Let us look at the pitfalls when the sales person has realised that you are looking for the cheapest policy.

He will reduce the IDV value by extra 10%. For instance, instead of IDV of Rs 11 lakh, he will give you quote for Rs 10 lakh. You feel the impact of this when the car is stolen. Then you will get claim based on Rs 10 lakh and not on Rs 11 lakh.

What a big loss of Rs 1 lakh while saving Rs 2,000?

In the liability part – not covering the passengers PA part. You feel the impact when the car is involved in major car accident and it is found that passengers sitting in the car are not covered.

Do we have a solution?

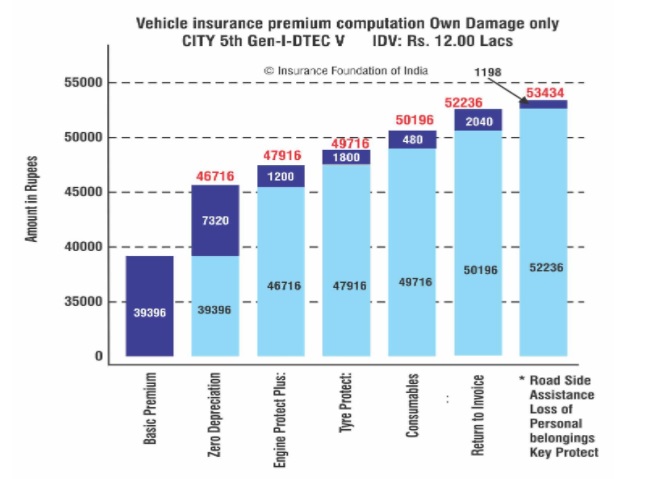

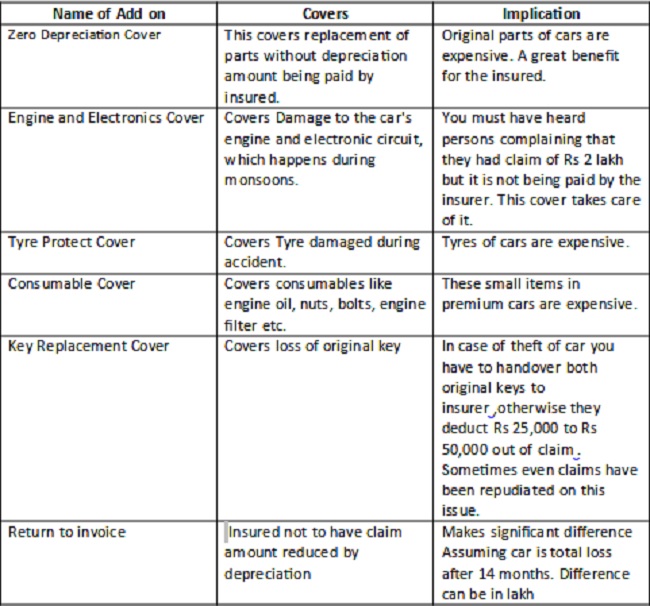

Yes, we have. Insurers have come out with add-on covers which specially take care of needs of those clients who have premium cars. Let us take a look at it:

From this histogram, you can see that addition of every add on is added to normal OD premium and as per your wish the premium of own damage insurance cost goes up from Rs 39,000 to Rs 54,000 but then you have to appreciate that you are insuring a car worth Rs 12 lakh. Engine seizure is a common claim during monsoons when you are stuck on a flooded road.

Your vehicle is a moving asset that is vulnerable to damage, theft and a substantial cost of repair or replacement. For premium cars this loss can be double due to the high cost of components as well as repair.

The comprehensive cover looks expensive upfront but works cheaper in the long term. Even minor accidents can cause significant damage to your car. This insurance shields you against such unexpected expenses.

When you buy a comprehensive cover with add-ons, then you buy full protection for your car, yourself and third party, in case of an unfortunate accident. Ultimately, it gives you peace of mind, on and off the road.

Learning: Time to come out of L1 Syndrome and insure your vehicle with add on covers. This will give you peace of mind. When you are a proud car owner then it is also time for you to upgrade yourselves. Car is prestige symbol for your family. Take care of it.

(The writer is director and founder of RIA Insurance Brokers. Views expressed are personal)