Atal Pension Yojana: Invest in the scheme before you turn 40

Atal Pension Yojana offers a guaranteed pension after the age of 60, provided monthly contributions are paid until the age of 60

Due to the impact of the coronavirus pandemic and growing awareness about financial security, people are moving towards long-term investment avenues. There has been a marked positive change in the mindset of people on building a robust retirement corpus and the Atal Pension Yojana (APY) is a scheme which fits the bill. APY is a government-sponsored social security scheme, which was launched in 2015. All bank account holders can join the scheme, which offers a minimum pension of Rs 1,000 and a maximum of up to Rs 5,000 a month. It offers a guaranteed pension after the age of 60, provided monthly contributions are paid till the age of 60.

Guaranteed returns

What makes APY popular is the guaranteed returns it gives in the form of pensions after retirement. It offers triple benefits of lifelong pension to the subscriber, lifelong pension to the spouse after the subscriber’s demise. Moreover, after the death of both of them, the entire corpus is returned to the nominee.

Taxability

Apart from the above three benefits, contributions are eligible for tax deduction up to Rs 50,000 under Section 80CCD (1B) of the Income Tax Act, which is additional to Rs 1.5 lakh allowed under Section 80C.

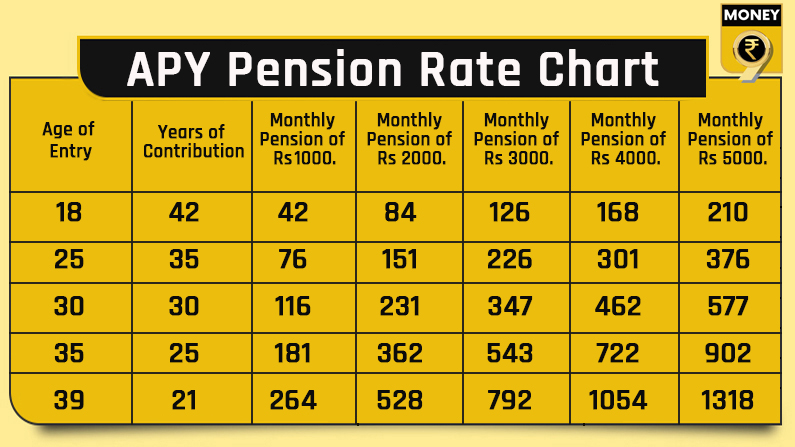

Net return

The amount of contribution to be made depends on your age, pension amount and the contribution period. For example, for the pension of Rs 5,000 a month, a 39-year-old person needs to contribute Rs 1,318 a month until the age of 60. After the contribution period of 21 years, the subscriber will get a lifelong pension of Rs 5,000. After the demise of the subscriber, the pension will be paid to the spouse. After their demise, the total corpus of Rs 3,32,136 will be returned to the nominees.

The back of the envelope shows that APY gives a net return of around 6.08% over the entire period of the policy. For the calculation, the average expectancy age is taken as 68 for the male, and the spouse’s assumed age is 71 years.

Fine print

— The scheme can be availed by all the individuals in the age group of 18 to 40 years. People above 40 are not eligible for the scheme.

— The subscribers can get a pension starting from Rs 1,000 a month to Rs 2,000, Rs 3,000, Rs 4,000 and Rs 5,000 per month after 60 years.

— The GoI guarantees the pension amount.

— Aadhaar will be the primary KYC.

— Banks are required to collect additional amounts for delayed payments varying from a minimum of Rs 1 to Rs 10 per month,

— In case of discontinuation of payment, the account gets frozen after six months, gets deactivated after 12 months and gets closed after 24 months.

Payout

On attaining the age of 60 years: The eligible pension amount would be paid to the subscriber.

In case of death of the subscriber: The pension amount would be available to the spouse, and on the death of both of them (subscriber and spouse), the pension corpus would be returned to his nominee.

Exit time: One cannot exit the scheme before 60 years of age. However, in exceptional circumstances, such as the beneficiary’s death or terminal disease, the exit is possible.

What to do?

APY is a good scheme for the low-income section. The maximum amount of pension is capped at Rs 5,000 which might not be sufficient for many if we take into account the inflation factor. APY can be considered to support your retirement as it gives the triple benefit of a lifelong pension to you and your spouse along with return of corpus to beneficiaries.