Debt funds vs Fixed Deposits: Check out tax efficiency

While safety holds supreme to conservative investors, taxes matter too. Consider post-tax returns when you are comparing two investment options

In a low interest rate regime, hunting for attractive investment options becomes challenging for conservative investors. While fixed deposits are the prime choice for them, they should consider debt funds too. If you put a lumpsum amount in a safer debt mutual fund, it will give you better post-tax returns in the long-term. One should not make an investment without tax consideration. Debt funds give you better post-tax returns compared to fixed deposits, especially when you are in the higher tax slabs.

The interest income on fixed deposits is taxed as per the income tax slab, i.e., at 20% or 30%. The bank also deducts tax deducted at source (TDS) at 10% if interest income for senior citizens exceeds Rs 50,000. What you must know here is if you did not file your income tax returns (ITR) for the last two years and your interest income was more than Rs 50,000 per annum, this year onwards the TDS will be deducted at 20%.

Tax-efficiency

The taxation in debt funds is simpler and more tax-efficient, especially when you hold it for more than three years.

First thing first, there is no TDS on selling or redeeming from debt funds. The tax is levied only on the capital gains. The short-term capital gains (STCG) tax as per your slab rate is levied on withdrawals up to three years. The long-term capital gains (LTCG) tax is levied at 20 per cent on withdrawals after three years. The LTCG at 20% also takes into account indexation benefit. Indexation benefit increases the cost of acquisition (your buying price) factoring in inflation, that reduces the taxable gains for you — hence you end up paying low tax.

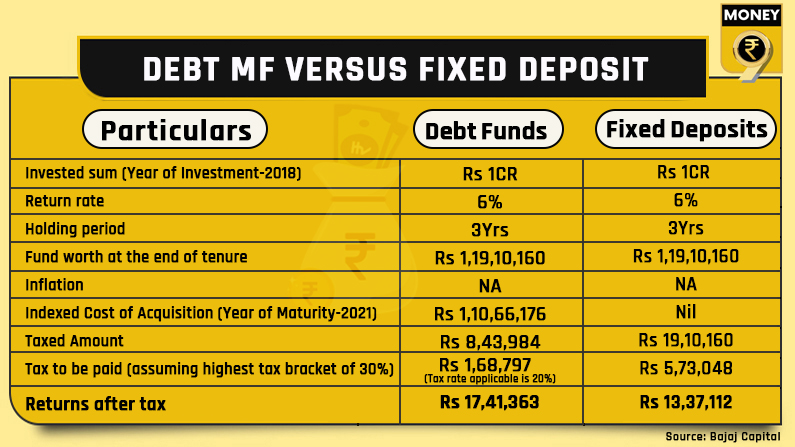

Take, for example, you invest Rs 1 crore in FD and in a debt fund. The interest rate you get on both is 6% and the holding period is three years. Both will have funds worth Rs 1,19,10,160 at the end of tenure. In case of FDs, the interest income of Rs 19,10,160 will be taxed at 30% rate (assuming the person falls in the highest tax slab). This amounts to Rs 5,73,048. The returns after tax comes out at Rs 13,37,112.

In case of debt mutual fund, Rs 19,10,160 capital gains will get indexation benefit. The taxable capital gains will amount to Rs 8,43,984. Now this amount will be taxed at 20%. Tax to be paid – Rs 1,68,797. The returns after tax stands at Rs 17,41,363, much more (Rs 4,04,251) than what you get in FDs.

While safety holds supreme to conservative investors, taxes matter too. Consider post-tax returns when you are comparing two investment options.

Download Money9 App for the latest updates on Personal Finance.