Freewheeling thoughts on financial freedom: Celebrating India’s 75th Independence Day

Before one takes the plunge into the vast ocean of investments, it is important to understand the difference between risk and volatility

While we commemorate a truly momentous milestone, the diamond jubilee year of our cherished independence, we must also introspect on an extremely vital but invariably overlooked aspect of our independence, which is financial independence. No wonder, only a small percentage of Indians can claim to be financially secure, even after the passage of 74 glorious years since India’s freedom.

Although managing finances is an integral part of our lives, many among us do it in reactive fashion. At best, they keep track of their debits and credits and try to set aside a certain amount for the rainy day.

Given this largely mechanical approach, it is no surprise that they are unable to cope with the financial pressures of key life goals and milestones like marriage, higher education, vacations, and retirement, leave alone emergencies. More often than not, financial ignorance leads one to a vicious cycle of financial doom: lack of knowledge leads to indiscipline, which in turn makes one vulnerable to monetary losses and mounting debt, as also the lure of quick money promised by unscrupulous market players.

The newest generation, the ‘zoomers’ born between 1997 and 2012, popularly known as GENZ, should be wary of this vicious cycle and resolve to become financially independent through prudent management of their money matters. This generation is digital by choice and lives life in DIY mode with no inhibitions whatsoever. They use social media not only for casual conversations but even for investing in stocks and cryptocurrency. They are convinced about the measurable value of stock market investments, having witnessed the progressive rise in Sensex and Nifty even during pandemic times, and they also find online investing simple and convenient.

Numbers bear testimony to the well-defined priorities of India’s younger populations. According to a recent survey by credit payment startup Slice, 57% of the respondents in the age group 18-30 are keen to make better investing choices while 21% would like to improve their saving habits. The most popular and least popular investment options for them are mutual funds and gold respectively.

In fiscal year 2020, the tier-2 and below contribution to cash turnover of BSE and NSE rose from ~30% to ~40% and ~14% to ~17%, respectively. The growing investor interest pan India was led by the younger population of over 20 and under 40. The percentage of customers from Tier-2 cities is today anywhere between 50% and 80% for tech-savvy platforms, an impressive leap compared to past figures.

No wonder, the fintech revolution has grown by leaps and bounds in India. According to a RBSA Advisors report, India is now Asia’s biggest destination for FinTech deals, with India’s total FinTech investments having crossed the $10 billion mark between 2016 and 2020.

Having said that, a key risk inherent in the freewheeling GenZ strides is the high degree of peer influence and often prejudiced social media advice that may guide key decisions including financial choices. Given their high intellect and intuition, these young minds can grasp key concepts in quick time provided the financial literacy happens in innovative ways. A good knowledge base can help them chart their success stories on the firm foundation of fiscal prudence and independence. The earlier this young brigade moves from impulsive spending to purposeful savings to prudent investments, the better would be their financial position and prospects.

Here’s a friendly Independence Day mini-primer for our independent-minded GENZ investors, a small step towards grasping the essence and significance of financial freedom.

Before one takes the plunge into the vast ocean of investments, it is important to comprehend and acknowledge one of its fundamental truths: the difference between risk and volatility. At times, investors have to endure long periods of lull, inaction and even negative growth before they reap the rewards of their stakes. Why does this happen? Because volatility is an integral part of investments, and volatility is not synonymous with risk.

Risk denotes the uncertainty of investment returns emanating from a host of factors including interest rate fluctuations, political uncertainty, credit risk, inflation, liquidity crisis and the like. Volatility, on the other hand, denotes the variations in investment value over time. This variation is not a risk if your investment is fundamentally strong.

An investor should hence strike a judicious blend of fixed-income investments and moderate to high-risk investments like stocks and mutual funds to ensure both growth and stability. The key is to find a judicious balance between risk and return though in a manner that protects your capital and boosts your wealth in the long run. One has the wherewithal to be prudently aggressive about money in one’s youth, when the risk appetite is higher, time frames are longer, and the income earning potential is progressively growing.

In the long run, your investment, more so in equities, will earn you a sizeable return, which is why the GENZ should begin investing as early as possible. One can start small and yet grow big, thanks to the power of compounding that beats inflation to build wealth, not income. The latter is always tied with expenses which invariably tend to grow at a faster pace than your earnings.

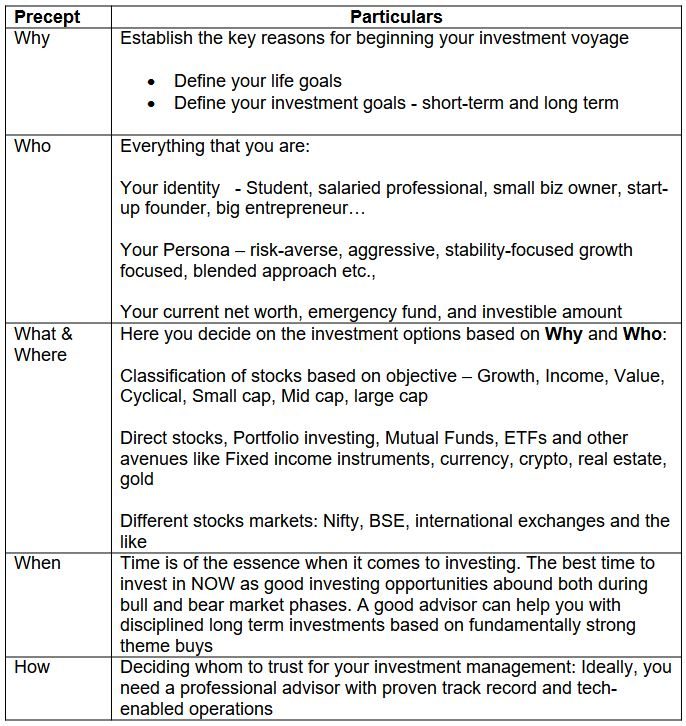

So, how to go about investing? By comprehending the 5Ws and 1H of investing.

5Ws and 1H at a glance

Following the 5Ws and 1H approach is easier said than done, even more so in these uncertain times of global challenges and disruptions like Covid-19. Hence the role of a competent and conscientious advisor can’t ever be over emphasised in helping investors with disciplined and diversified investing in line with income profiles and risk appetites, making the most of tax incentives and market opportunities. Good advice is also about protecting investors from the perils of excessive fear or greed while helping them make sense of market cycles, including sharp upswings and drastic falls.

One is never too young to manage finances. Given the right guidance, one can remove the stress and strain from financial management by beginning to make sense of it – from knowing how to arrive at their net worth and preparing budgets to deciphering risk-reward relationships and comprehending the universe of intricate financial products.

Here’s wishing the GENZ a fulfilling investment voyage. May they make the most of their treasured independence through a treasure trove of financial prosperity.

(The author is Head – Sales & Dealing at Yes Securities. Views expressed are personal.)