JM Financial NCD opens today. Should you invest?

NCDs are debentures that cannot be converted into equity shares at the time of maturity

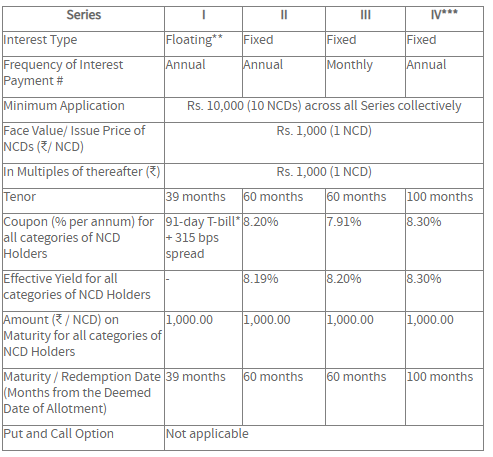

JM Financial Products, the NBFC arm of the JM Financial Group, has announced Tranche 1 of the public issue of secured non-convertible debentures (NCDs) with a fixed coupon rate of up to 8.30 per annum. There are 4 series of NCDs carrying fixed and floating coupons having tenure from 39 to 100 months with an annual and a monthly interest payment option. The tranche I issue opens on September 23, 2021, and closes on October 14, 2021.

NCDs are debentures that cannot be converted into equity shares at the time of maturity. They are classified as secured and unsecured. Secured NCDs have an advantage over unsecured NCDs at the time of liquidation but they carry a lower rate of interest compared to unsecured ones.

Vishal Kampani, managing director, JM Financial Products, said, “JM Financial Products has fortified its position across business verticals with a diversified product mix while maintaining a focus on risk-adjusted profitable growth. The Company has maintained strong liquidity buffers. This public issuance will continue to help us diversify our borrowing and investor mix. Our strong balance sheet, well-capitalised and diverse set of businesses and strategic client-focused approach position us to drive sustainable value for our stakeholders.”

The face value of NCD is Rs 1,000 each, with a base issue size of Rs 100 crore, with a greenshoe option of up to Rs 400 crore, aggregating up to Rs 500 crore.

Important info for investors

The press release states, “The Tranche I offers 4 Series – Series I comes with a floating interest rate option in the tenor of 39 Months. Series I carries a floating interest rate based on a 3-month T-Bill Rate published by the Financial Benchmarks India Pvt. Ltd. (FBIL) plus 3.15% spread. The coupon for series I NCDs will depend on the movement of the T-bill rate.”

“In addition, Series II, III and IV come with a fixed interest rate options in the tenor of 60 months (annual), 60 months (monthly) and 100 months (annual), respectively. Effective annual yield for Series II, III and III NCDs ranges from 8.19% to 8.30% per annum. The Tranche I issue offers options for subscription with coupon rates ranging from 7.91% to 8.30% per annum for Series II, III and IV NCDs (fixed interest rate).”

Credit rating

The issue has been rated [ICRA]AA/ Stable by ICRA and CRISIL AA/ Stable by CRISIL Ratings Limited.

Liquidity

The NCDs will be listed on BSE and investors can apply for NCDs only in dematerialized form.

Taxability

Interest income will be charged to tax as “Income from Other Sources” at the rates applicable to the investor. If sold before maturity within one year of buying then short term capital gain tax is levied, which is taxed according to the marginal tax rate. If sold after a year, 10 % long term capital gain tax is levied without indexation.

What should investors do?

Investors with a higher risk appetite can invest from a returns perspective. For similar investments, one can also consider diversifying their investments through credit risk mutual funds which invest in low-credit quality debt securities.