Know what are the additional tax benefits for senior citizens

Senior citizens may claim a larger deduction of up to Rs 50,000 for premiums paid on medical insurance policies under Section 80D

Elderly taxpayers benefit from greater tax incentives and rebates under the old income tax regime compared to younger taxpayers. However, under the new income tax regime introduced in Budget 2020, individuals are not classified according to their age. As a result, the old income tax regime contains various sections that provide benefits and rebates to senior citizens. Under the old regime, there are various exemptions, deductions on interest income that the senior citizen gets.

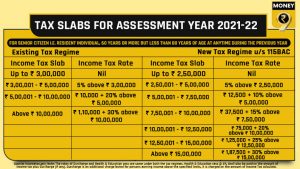

Senior citizens between the ages of 60 and 80 have no tax liability up to Rs 3 lakh and super senior citizens up to Rs 5 lakh. In comparison, individuals under the age of 60 have a taxable income threshold of Rs 2.5 lakh. (See the tax slab table).

Apart from various popular deductions, there are also additional benefits that a senior citizen should be aware of. Let’s take a look at what are the benefits as per rules.

Relief from an advance tax

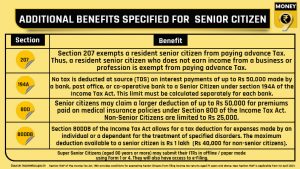

According to Section 208, any individual with an expected tax burden of Rs 10,000 or more for the year shall pay his tax in advance, in the form of advance tax. However, section 207 exempts a resident senior citizen from paying advance tax. Therefore, a resident senior citizen who does not earn income from a business or profession is exempt from paying advance tax.

Income tax deduction

The Income Tax Act, section 80TTB, provides tax benefits on interest earned on deposits with banks, post offices, and co-operative banks. The deduction is available for interest income up to a maximum of Rs 50,000 generated by the senior citizen. Interest earned on both savings and fixed deposits is deductible under this rule.

Additionally, under section 194A of the Income-Tax Act, no tax is deducted at source (TDS) on interest payments of up to 50,000 made to a senior citizen by a bank, post office, or co-operative bank. This limit must be calculated separately for each bank.

Tax benefits on medical insurance

Senior citizens may claim a larger deduction of up to Rs 50,000 for premiums paid on medical insurance policies under Section 80D of the Income-Tax Act.

Additionally, Section 80DDB of Income-Tax Act allows for a tax deduction for expenses made by an individual or a dependent to treat specified disorders. The maximum deduction available to a senior citizen is Rs 1 lakh.

Filling ITR

When it comes to super senior citizens, they may submit their ITRs offline, i.e., paper mode using Form 1 or 4. They also have access to e-filling. Going forward from the fiscal year 2021-22, section 194P of the Income-Tax Act, 1961 provides conditions for exempting senior citizens from filing income tax returns aged 75 years provided they fulfil certain conditions. The new section would be applicable from April 1, 2021.