Retirement planning: Should you invest in mutual funds?

Retirement mutual fund plans typically invest in low-risk investment options such as government securities

When it comes to retirement planning, the savings instruments that often come to mind include pension plans from insurance companies, National Saving Certificates (NSC), Employee Provident Funds (EPF), and Public Provident Funds (PPF). Many of us fail to create sufficient retirement plans and wind up relying on our family to take care of us. However, if you are not afraid to take a little risk with your money, mutual funds are an excellent retirement investment.

According to the Association of Mutual Funds in India (AMFI), the fourth category of mutual funds is called ‘Solution-Oriented Schemes’. The retirement fund is part of this category; let’s look at the features of the retirement fund and whether you should invest?

Retirement fund

Retirement funds, alternatively referred to as pension funds, are financial vehicles that enable individuals to set aside a portion of their income for retirement. After retirement, these funds provide a steady source of income; a retiree receives an annuity on their investment until their demise.

Pension funds are invested on behalf of investors, and the revenue generated by those investments is given to the pool of funds in the form of interest.

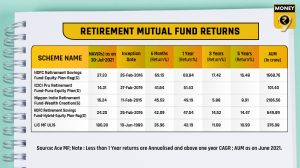

To achieve consistent returns, retirement mutual fund plans typically invest in low-risk investment options such as government securities.

Taxation aspect

Contributions to retirement mutual funds are tax-deductible up to a maximum of Rs. 1.5 lakh (under Section 80CCC). These payments may involve purchasing a new pension plan or the renewal of an existing fund to maintain its services. Withdrawals, on the other hand, are tax-deductible.

Because the money is distributed as an annuity, it attracts tax depending on the existing rates. That said, the pensions that are paid on a periodic basis are completely taxable on an individual’s salary tax slab. However, if an individual elects to distribute the entire balance post-retirement, the individual’s tax policy may change.

Should you invest?

The fundamental objective of a retirement savings fund is to provide a steady stream of revenue for an investor during the absence of income. It can be viewed as deferred pay, providing individuals with financial security and sufficient capital to meet their basic needs.

The majority of pension funds give the option of receiving payouts as a monthly annuity or as a lump sum.

Monthly annuities are paid at a fixed rate, which includes inflation protection in the majority of cases. It is one of the most significant benefits since investors receive their retirement fund’s return adjusted to the current denomination.

The lump-sum payments distribute the investor’s whole accrued wealth. While it provides vital financial backing, it eliminates the regular source of return associated with monthly annuity payments.

There are essentially three different plans available. The most popular plan invests exclusively in debt profiles, making it incredibly safe and suitable for conservative borrowers. Additionally, there are unit-linked plans that invest equally in equity and debt profiles. These carry a slightly more significant risk but also offer higher returns.