Struggling to start your SIP journey? Here's how you can go about it

To reiterate, a financial goal has three components – Purpose, Amount and Time. As a first step, it helps to list all your goals.

As we have discussed before, goal-based investing is the best way for you to reach your financial goals. Writing and tracking financial goals actually fuels the commitment required to achieve them.

In this post, we discuss how unified goal planning helps you achieve your goals by investing less today. Unified goal planning takes all your financial goals and calculates one SIP amount you need to invest by optimising across all goals. The combined SIP in a unified goal approach is less than the sum of the individual SIP required to achieve the goals separately.

To reiterate, a financial goal has three components – Purpose, Amount and Time. As a first step, it helps to list all your goals.

Let us look at the following example:

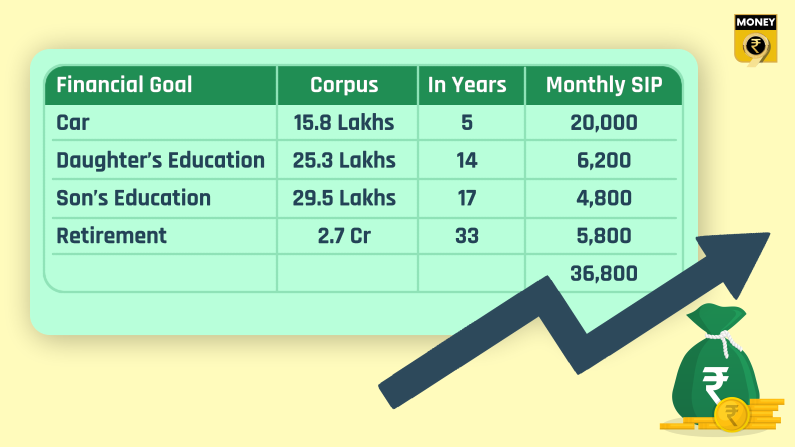

A 27-year-old with a current monthly expense of Rs 45,000 is planning for the following goals:

Your set of goals will be specific to you, so treat the above as an illustration. Part of a good goal planning system is to calculate how much you need to invest today. These calculators, popularly called SIP calculators, tell you the amount needed to be invested each month to achieve your financial goals.

Here is what our goal calculators show as SIP for the above goals –

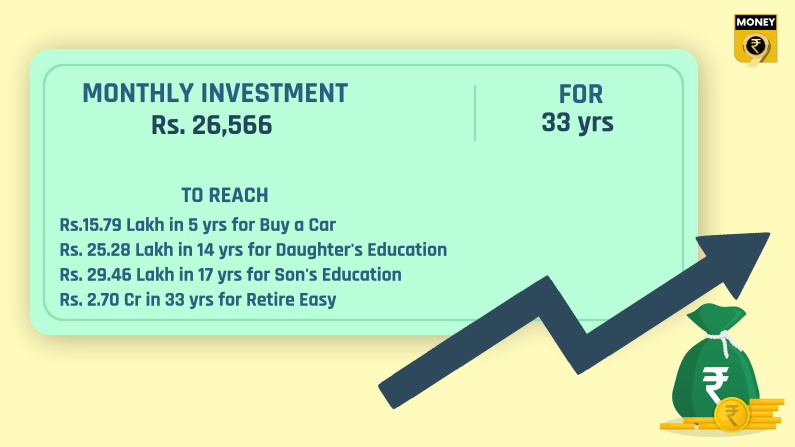

So if you plan for all the goals separately, you need to start investing Rs36,800 today. If you used a unified goal planning approach, the SIP required would be much lower. Rs 26,600 a month in this case. With a unified portfolio approach, you start with a SIP amount that is 28% lower and still have the same set of goals.

How does this really work?

Let’s simplify and see the math behind this.

Say, you have two goals

Goal 1 – Requires SIP of 5,000 for 5 years

Goal 2 – Requires SIP of 10,000 for 10 years

A simple advice would be investing Rs 15,000 for five years and then Rs 10,000 from year 5 to 10.

Notice this:

- Your SIP amount is not constant for 10 years

- You are being asked to invest more now and less later. Your income, on the other hand, is likely to increase over time. Regardless if you can invest Rs15k today you can invest Rs 15 five years from now, so you shouldn’t be asked to decrease your SIP amount.

Using a unified goal planner, you can invest Rs 12,000 every month for 10 years to achieve both goals. So start smaller today and never change your SIP amount. Isn’t that more intuitive?

(The writer is CEO and founder, Kuvera.in. Views expressed are personal)