Fixed deposit fixation is injurious to wealth

Balanced Advantage Funds will give high single-digit or even double-digit growth in five years, experts believe

Fixed deposit investments could be injurious to long-term wealth creation if present rates of low interest and high inflation are to stay. The covid-19 pandemic is not making matters any better for the foreseeable future.

With retail inflation hovering at 5.5% levels, fixed income investment products are unable to yield wealth creation opportunities for investors. Most banks offer fixed deposit rates lower than or just at par with inflation. But add to that (or subtract from that) the tax liability on FD interest and investors are left with negative growth on their money. Simply put, 100 rupees invested in fixed deposit at present interest and inflation rates (both calculated at 5.5%) will be worth approx. 130 rupees in five years – enough to buy goods and services presently available at 100 rupees (or 130 rupees in five years).

But with a 30% tax on interest on this Rs 130, the amount available to an investor reduces to 120 rupees. Not nearly enough to but 130 rupees worth five years from now. That’s money depreciated.

Experts believe Indians will need to include a healthy dose of equity in their portfolios for creating wealth. One way to do it is by investing through Mutual Funds. However, with hundreds of funds available in the market, crunching data for an investor is difficult as not many consult professional financial advisors.

One filter while searching for investment options during the present market volatility could be looking at balanced advantage funds, or Dynamic Asset Allocation Funds.

“In a very volatile market, like today, if one is not clear on what asset allocation suits him/her the best, one should consider investing in dynamic asset allocation funds as these funds can provide stable returns with a mix of equity and debt,” said Feroze Azeez, deputy CEO of Anand Rathi Private Wealth.

Aashish P Somaiyaa, CEO of White Oak Capital concurs. “If you look at Balanced Advantage Funds, they are an excellent opportunity for conservative investors who don’t want to put all their money in fixed income buy at the same time don’t feel comfortable going the whole hog in 100% equity,” he says.

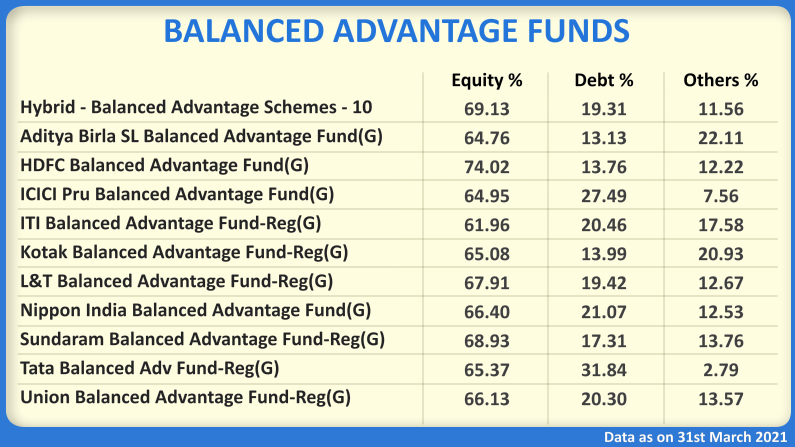

These hybrid mutual funds offer a mix of equity and debt both in the same fund to ensure growth as well as safety of capital. Here are 10 Balanced Advantage Funds with their exposure to equity, debt and other investment categories (gold, real estate etc) as on 31st March 2021.

10 Balanced Advantage Funds

Somaiyaa says such funds have the advantage of calibrating and recalibrating equity exposure and fixed income exposure depending upon valuation indicators and ‘cheapness’ or ‘expensiveness’ of the market. “Balanced Advantage Funds are a great opportunity to get high single-digit or double-digit returns over a five-year period with low volatility. It is ideal for someone who is risk-averse in taking direct equity exposure,” he said.

These funds adjust the level of equity in line with the markets. As the market levels go up, their allocation to equity comes down; and as market gets cheaper, they increase their equity allocation.

“In March 2020, when markets fell, these funds increased their equity weightage to 90% and have been reducing post the markets rallied,” Azeez said.