MF expense ratio: Why you should not turn a blind eye to it

MF investments: Expense ratio is calculated and charged daily since it has to be adjusted in the NAV. A fund house deducts the expenses ratio even before the investment is added to the pool of funds

Financial experts and the mutual fund industry have been very vocal about the fact that investments in mutual funds enjoy the benefit of power of compounding. But what they have been silent about the fact that your expenses for managing those funds also compound. Our analysis shows that the total expenses work out to Rs 25,101.44 or 25% of the investment amount paid by an investor on an investment of Rs 1,00,000 in a fund with a rate of return of 10% and an expense ratio of 1.5% over 10 years. Surprised? So, let us understand this in detail and start with the basics.

What is Expense Ratio?

Under SEBI (Mutual Funds) Regulations, 1996, Mutual Funds are permitted to charge certain operating expenses for managing a mutual fund scheme. These expenses include sales & marketing/advertising expenses, administrative expenses, transaction costs, investment management fees, registrar fees, custodian fees, audit fees – as a percentage of the fund’s daily net assets. All such costs for running and managing a mutual fund scheme are collectively referred to as ‘Total Expense Ratio’ (TER).

In short, it is a fee that you pay for managing your money professionally which deducted as a percentage of your investment amount. It is calculated as a percentage of the scheme’s average Net Asset Value (NAV). The daily NAV of a mutual fund is disclosed after deducting the expenses.

How is the expense ratio decided?

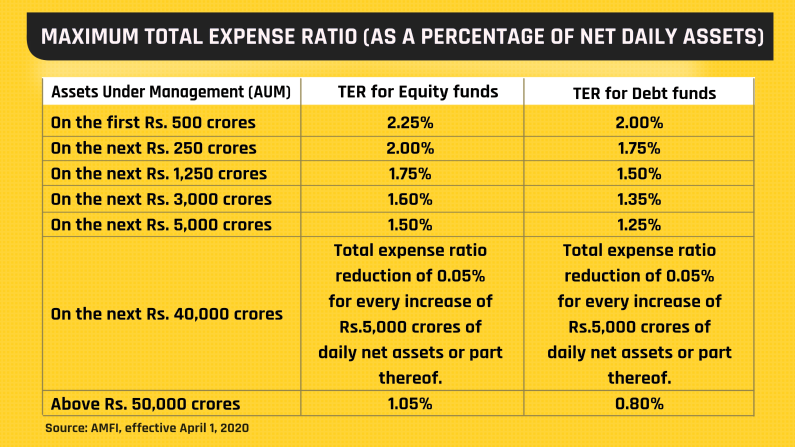

The value of an expense ratio depends upon the size of the mutual fund in question. If the funds’ assets are small, then the expense ratio can be high. Similarly, if the net assets of the fund are significant, then the expense percentage should ideally come down. However, these expense ratios should be charged based on SEBI’s rules and regulations for the Total Expense Ratio (TER). Effective from April 1, 2020, the TER limit has been revised as follows.

In addition, mutual funds have been allowed to charge up to 30 bps more, if the new inflows from retail investors from beyond the top 30 cities (B30) cities are at least (a) 30% of gross new inflows in the scheme or (b) 15% of the average assets under management (year to date) of the scheme, whichever is higher. This is essentially to encourage inflows into mutual funds from tier-2 and tier -3 cities.

The math

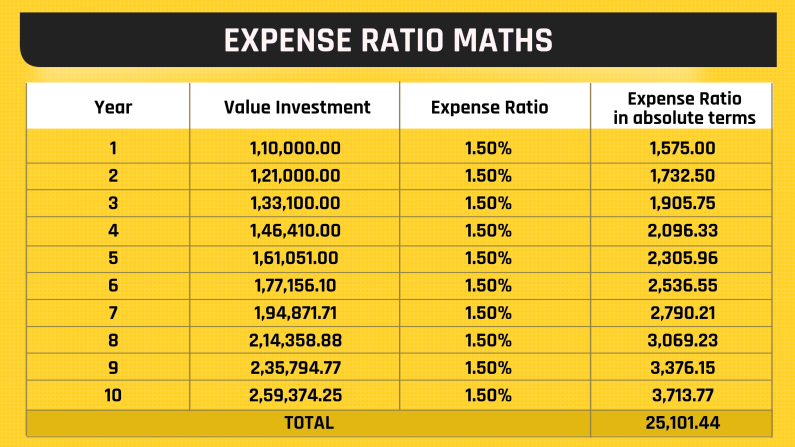

Now that you have understood what the expense ratio is, how is it decided. Let us understand how it compounds over time. For the sake of simplification let’s assume that you plan to make a lumpsum investment of Rs 1,00,000 in a mutual fund with an expense ratio of 1.5% and the fund delivers 10% returns every year for 10 next years. The below matrix shows the value of your investment at the end of each year. While the expenses ratio in absolute terms is calculated based on the average of investment that is (opening value of investment + closing value of investment)/2*1.5%. So, for the first year it works out to be Rs 1,575 = ((1,00,000 + 1,10,000)/2 * 1.5%)

The above matrix shows that an investor ends up paying Rs 25,101 or 25% of his investment corpus as expenses to a fund house. While the 1.5% expenses ratio as a ratio seems minuscule on the face of it but when looked at in absolute terms and totality, the number is big enough.

While calculating returns you will be told that your investment of Rs 1,00,000 has turned into Rs 2,59,374 with a compounded annual growth rate (CAGR) of 10% but in reality, the fund has grown at a CAGR of 12.32%. The 2.32 percentage points difference is due to expenses deducted by the fund house.

One of the prime reasons this number stays hidden is because the expenses ratio is deducted before the calculation of the net asset value (NAV) of a fund. Let us now understand how the expenses ratio is charged.

How is expense ratio charged?

The expense ratio is calculated and charged daily since it has to be adjusted in the NAV. A fund house deducts the expenses ratio even before the investment is added to the pool of funds. Continuing with the same example. When you invest Rs 1,00,000 in a particular fund the asset management company will deduct the expense ratio and transfer to the pool amount will be Rs 99,995.89 as Rs 4.11 (1,00,000*((1.5/100)/365))) is charged as the expense for the day.

Since the expense ratio levies a burden on annual returns earned, as an investor you should carefully analyze the same while choosing a mutual fund scheme to invest in.

Just like in other things we look at the cost but take a decision based on many other aspects like quality of the product, its durability. Similarly, in mutual funds, it’s important to look at the expenses ratio but the overall decision should be also based upon many other things. Remember, a good fund delivers good performance with optimal expenses.

“Investors who are very cost-conscious need to do is evaluate whether they want to go to index funds and whether their fund managers are generating enough alpha to justify their expense,” said Vishal Dhawan, founder and CEO at Plan Ahead Wealth Advisors.