Why ELSS should be part of your portfolio

Compared to other tax-saving products like PPF , tax-saving FD and NSC with a 5-year lock-in, ELSS stands out due to its relatively lower lock-in period of just three years, all while generating higher returns

Consider a financial route that lowers your tax burden and opens the door to wealth accumulation. Enter ELSS, the Equity Linked Savings Scheme, where the thrill of the stock market meets the world of tax-saving investments.

ELSS, frequently touted as the “superhero” of tax-saving tools, is not your typical investing choice. Entering the world of stocks, where measured risks meet possible returns, is a risky move that investors should understand before investing.

What is an equity-linked Savings Scheme?

Equity Linked Savings Scheme, or ELSS, is a type of mutual fund investment that falls under the Equity category of mutual funds. The fund manager invests at least 80% of the investment in stocks.

Compared to other tax-saving products like PPF (Public Provident Fund) with a 15-year lock-in period, tax-saving FD (Fixed Deposit), and NSC (National Savings Certificate) with a 5-year lock-in, ELSS stands out due to its relatively lower lock-in period of just three years, all while generating higher returns.

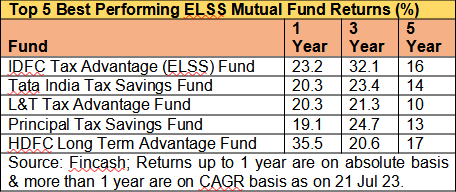

These funds are known for their diversification and historical track record of delivering favorable returns compared to other tax-saving options. As per value research ELSS have given an average return of 19.38%, 23.45% and 12.89% respectively over 1,3 and 5 years respectively as of 25th July, 2023.

Source: Fincash;

Returns up to 1 year are on absolute basis & more than 1 year are on CAGR basis as on 21 Jul 23.

Risk of investing in ELSS:

ELSS funds invest a substantial portion of their capital in stocks, making them susceptible to market fluctuations.

The value of equity investments can rise or fall based on economic conditions, corporate performance, global events, and investor sentiment, among other variables.

The NAV (Net Asset Value) of ELSS funds can be affected by market volatility, resulting in potential gains or losses for investors.

If an investor requires liquidity for an emergency or any other reason, they cannot withdraw their ELSS investment until the lock-in period expires.

Should you invest in ELSS?

Investors may deduct up to Rs. 1.5 lakh from their taxable income in a financial year by investing in ELSS, which offers tax benefits under Section 80C of the Income Tax Act.

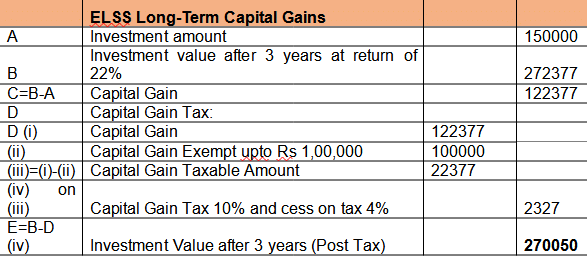

ELSS has a mandatory lock-in period of three years. That means after 3 years, any gains of up to Rs 1 lakh a year are tax-free, and any gains over this limit will attract a long-term capital gains tax at 10% plus applicable cess and surcharge.

Below is an example of how much investment value is left after three years post-taxation on capital gains that are above Rs 1,00,000.

Investors can make contributions to ELSS funds via SIP (Systematic Investment Plan), fostering a habit of regular investing and improved financial planning. Most other tax-saving products lack a systematic monthly investment option. It’s important to note that ELSS funds attract a long-term capital gains tax of 10% upon sale, unlike PPF interest, which is tax-exempt,” said Raghvendra Nath, MD, Ladderup Wealth Management Pvt. Ltd.

Conclusion

It is pertinent to remember ELSS is still a high-risk mutual fund product. To reduce risk, investors should diversify their holdings, select ELSS funds with a proven track record and a proven investment strategy, and align their investment horizon with their financial objectives.

Additionally, consulting a qualified financial advisor can aid investors in making informed decisions and effectively managing risks.

Even though ELSS investments generally have a minimum lock-in of three years, linking these investments to your longer-term goals is still beneficial. Keep your investment horizons longer and be patient to get favorable outcomes.