Compounding: Nine things you should know

Compounding can do wonders if one starts investing early. One does not have to be a financial expert to gain from the benefit of compounding

Albert Einstein had said: “Compound interest is the eighth wonder of the world. He who understands it, earns it, he who doesn’t pays it.”

All of us have learnt the concept of simple interest and compound interest in high school.

In this article, we will talk about eighth wonder of the world along with rupee cost averaging approach which can be a ninth wonder.

How does compounding work?

Compounding is referred to as earning interest on interest.

Assume that you invest Rs 5,000 for 10 years at 12% interest rate.

At the end of the year 1, you will earn Rs 600. This will grow your invested amount to Rs 5,600.

At the end of year 2, you will earn Rs 672 which will raise your invested amount to Rs 6272.

This will go on and on…

At the end of the 10th year, you will earn Rs 1,664 and while your initial investment of Rs 5,000 would grow to Rs 15,530.

Thus, compounding is a continuous process in which returns are generated on the returns until the time your money remains invested.

How to gain from benefit of compounding?

You all must be wondering when should you start investing? Is it when you get your first pocket money or when you get a job or when you get married? Well, the simple answer to this question is start investing as early as you can.

Start early, start young

With early investing comes the power of most scarce resource which cannot be bought i.e., time. With time and power of compounding, you can create wealth.

Here’s an interesting story.

Warren Buffet, who is widely known as one of the successful investors, started investing just at the age of 11. He bought his first stock at 11 and at the age of 15 he had a net worth of $6000 which is quite impressive. Taking motivation from this story, everyone should start investing early to reap the benefits of compounding.

In the image below, we can see that Veer has started investing early whereas Vyom started investing 15 years after Veer started. As seen in the image, Veer is generating returns on the initial returns, because of power of compounding. This means that Veer got a head start which is hard to beat – accumulating Rs 7.77 crore versus Rs 3.25 crore starting 15 years later. In spite of Vyom investing more than 3 times of Veer, he still couldn’t catch up.

One of the important reasons to start investing early is power of compounding.

Lump sum or SIP — What to choose?

The power of compounding is more amplified in SIP investing vs Lumpsum.

Disciplined investing approach

The investor must make periodic investments rather than investing all at once. This is called disciplined investing. Being regular in investing, would pay off in the future with the benefit of compounding.

Patience is a virtue

Lots of investors want quick returns. Chasing quick returns is not the right strategy to pick. Long term investing is. Power of compounding works well for long term investing. Patience plays a crucial role while investing for long term. Only with patience, the investor can reap the benefit of compounding.

Rupee cost averaging approach

One of the strategies that gives good returns is “buy when the markets are low and sell when the markets are high.” But how can one know when the markets have hit the lowest point? This is where rupee cost averaging approach plays an important role.

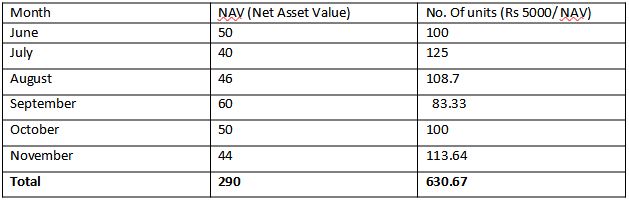

To understand rupee cost averaging approach, assume that you are investing Rs 5,000 every month, starting the month of June for 6 months, in an equity mutual fund scheme. Due to high volatility present in equity mutual funds, NAV (Net Asset Value) keeps on fluctuating. There is a very low chance that you will be able to invest at the same NAV every month. Look at the illustration in the table below to understand the concept better:

In the table above, the average purchase price of mutual fund units for six months is reduced to Rs 48.33 (290/6). Total units bought are 630. Let’s say you chose lumpsum investing instead of SIP in the month of June, then in such a case, your purchase price would be Rs 50 (NAV). You would have received 600 units (investing Rs30,000 at once for 6 months, so (Rs 30,000/50) = 600 units.

SIP investing happens both at the highs and lows of the market. Whereas in lumpsum investing there is a risk of entering the market at a high. SIP investing helps in managing anxiety of the investors.

Conclusion

Compounding can do wonders if one starts investing early. One does not have to be a financial expert to gain from the benefit of compounding. As we saw that the power of compounding amplifies with long-term investing, one should be patient and invest for long term. It is also important to be disciplined investor to gain the maximum benefit of compounding. Rupee cost averaging is a wonderful approach used for hedging when the markets are falling downwards. It does not guarantee returns; however, it reduces the risk of investing in volatile markets.