Personal loan: Here are top-9 banks with lowest rates

You need to decide if you want a loan from your primary bank where you receive your salary and have fixed deposits, etc, or an entirely new bank

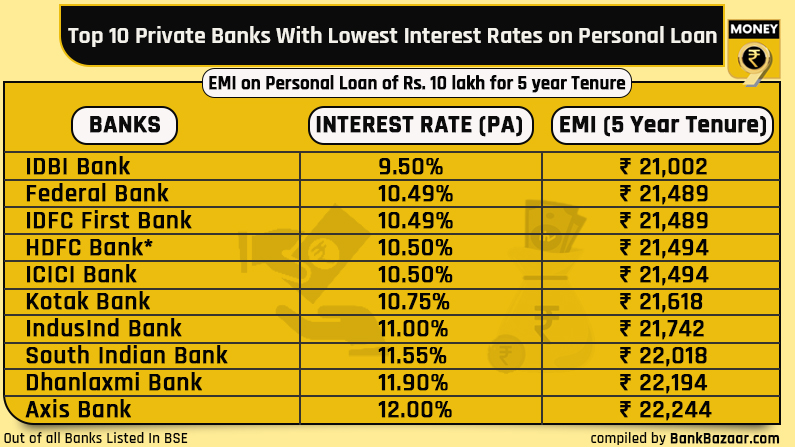

The precarious financial situation post Covid-19 forced many to take personal loan. There are others who may want the money to fund other needs such as buying consumer goods, car or home. If you are looking for personal loan and trying to figure which banks to go for, we have collated a list for you. Below are Money9’s picks – in collaboration with Bankbazaar.com – of top 9 public and private sector banks with lowest interest rates on personal loan:

Look beyond rates

Interest rate indeed plays a significant role when you go for a personal loan. But this is not the beginning and end of it. There are other factors to look at.

“Borrowers only enquire about interest rate and EMI amount. Very few of them factor in processing charges, pre-payment and late payment fees. Even more caution is needed if a new-age fintech is at the forefront of a bank. For example, you might be dealing with a smart fintech with an RBL Bank or a YES Bank behind it. You should be aware of what you are signing for,” says Amit Das, CEO and co-founder, Algo360, a credit score analyser firm.

Primary bank versus a new bank

You need to decide if you want a loan from your primary bank where you receive your salary and have fixed deposits, etc, or an entirely new bank. The following anecdote is crucial to keep in mind.

Sudha Gupta (name changed) lost her husband during Covid-19. She was a nominee in her husband’s savings bank account but not a co-applicant in an unsecured loan that was running. When she called the bank to take forward the paperwork, the first thing they did was freeze all the deposits. “Legally she was not liable to pay the money because it was an unsecured loan, but when you take loan from your primary bank you are running the risk of getting your money blocked in case you fail to pay the EMIs,” says Das.

Taking a loan in your primary bank account, from convenience point of view, appears better, but you need to consider consequences. “In case your assets get frozen it will be double whammy. First, you’ll lose access to your savings for your daily needs. Second, since you are unable to payback loan, your credit score will take a hit,” says Das.

This is again a matter of convenience. Private banks will have better customer services, while public banks may need you to visit the bank for every other task. However, interest rates are indeed cheaper at public sector banks. “It is easier to navigate up in hierarchy in private banks and a mammoth task with public banks. Most of the times, bankers at front desk will not be aware of a solution to the specific challenge you are dealing with. Nevertheless, public banks are much more empathetic. They follow terms and conditions. The recourse with the regulator is easier if you have issues with a public bank. If you have time and patience to deal with the slow execution, go with public banks,” says Das.