Stay away from stress of tax and financial planning, all at once

For most of us, retirement might seem like a far cry. But if you start saving for your twilight years right away, not only will you benefit then, but you will also save a great deal on your taxes right now.

This tax season had been a whirlwind for Abhinav. He had haphazardly rushed through the process, missing crucial documents like Form-16 and salary slips. Moreover, he only narrowly made it to the 31st July ITR filing deadline, managing to file returns without penalties.

A software engineer by profession, the 30-year went the do-it-yourself (DIY) route for ITR filing. But upon closer inspection of his returns by his friend, who was a professional CA, he realized that he could have slashed his tax liabilities significantly, had he not rushed at the last minute, made some mistakes, not chosen the default new regime and claimed some beneficial exemptions.

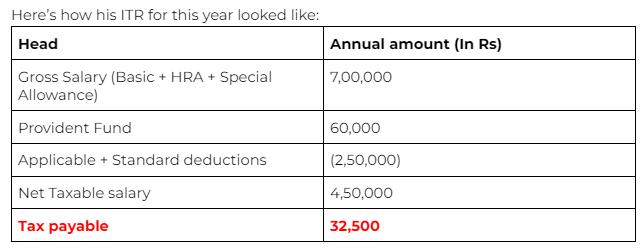

Here’s how his ITR for this year looked like:

If you’ve found yourself in a similar tax-filing soup like Abhinav’s, fret not. No, you cannot undo your previous financial mistakes now, but you can be well prepared for the next one. Here are some errors that Rajeev, and you, can avoid next time you’re filing your taxes.

Don’t discount NPS

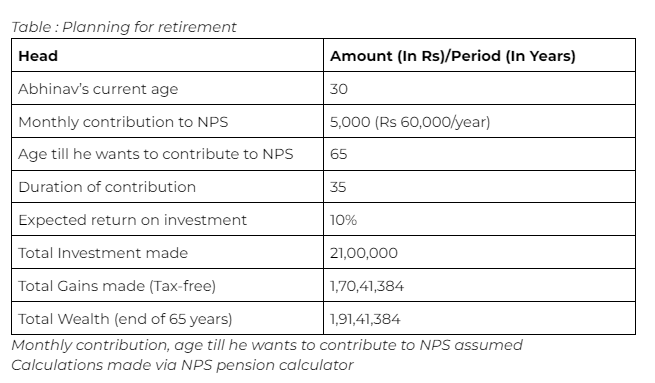

For most of us, retirement might seem like a far cry. But if you start saving for your twilight years right away, not only will you benefit then, but you will also save a great deal on your taxes right now.

A salaried employee’s contribution towards his/her NPS account is eligible for tax deduction of maximum Rs 1,50,000 under Section 80CCD (1). Additionally, one can claim a deduction of Rs 50,000 over and above this limit in lieu of their personal contributions to an NPS account, under Section 80CCD (1B). So, all in all, an individual can claim tax deductions of up to Rs 2 lakh in a financial year.

Moreover, investments in NPS are market-linked. This means that your funds are invested across asset classes like equity, debt and others, depending on your risk appetite, whether aggressive, moderate or conservative. And they will grow as the stock market inches up, or go down.

The 10-year returns on equity in tier-1 accounts (only ones eligible for tax benefit) ranges between 10.45%-10.86%. Tax protection, plus handsome returns, right there!

ELSS up your finances

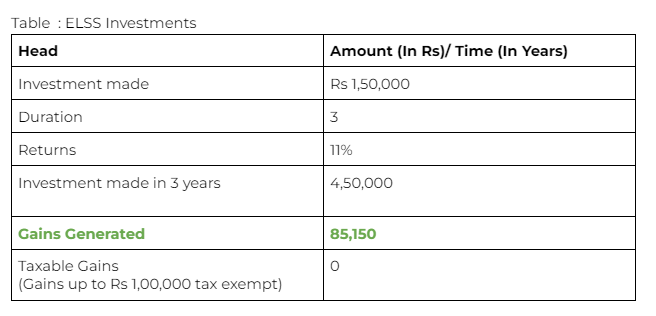

Investing not just for retirement, but for other major life goals is also crucial. For that, Equity Linked Savings Scheme (ELSS) can come in handy. They are the mutual fund category that get tax benefits. They invest at least 65% of their portfolio in equity instruments and have a lock-in time of just 3 years, post which you can withdraw your funds.

So, had Abhinav invested Rs 1,50,000 (maximum limit in an year i.e. Rs 12,500/month) in these mutual funds, along with saving on tax, here’s how much he would have made:

Your premiums can help, too

Retirement protection, investment and finally, insurance. You can claim tax deductions for premiums on life insurance policies you’ve paid for yourself, your dependent senior citizen parents, and your spouse. If both parents are senior citizens, then you will be eligible for a deduction of up to Rs 50,000 paid as their policy premium. For yourself and your spouse, you can claims deduction of up to Rs 25,000

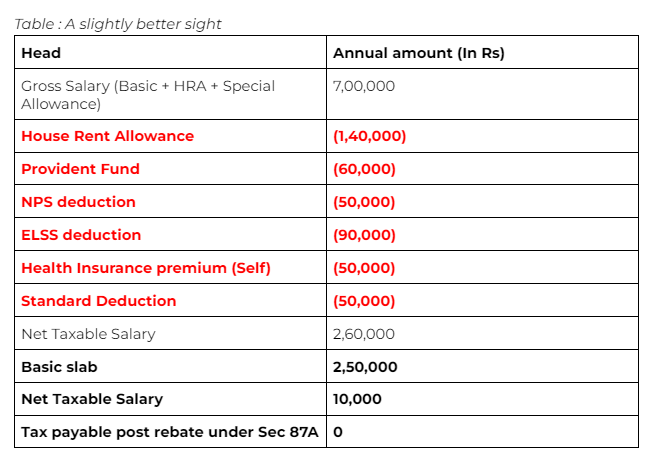

In all, had Abhinav claimed all these deductions, here’s how his ITR would’ve looked like:

Other common mistakes

Says CA Prachi Jain, “ If your income is more than Rs 2,50,000, you need to file your tax return even if your tax has been deducted at source. There is no exception. TDS is deducted on your salary income, but most of the time these individuals also have bank accounts, meaning they have FDs, and because of this they have interest income also. TDS is not deducted on that part. So it is also important to show that in the tax return and pay taxes on that”.