Diabetes can damage your body and pocket, both

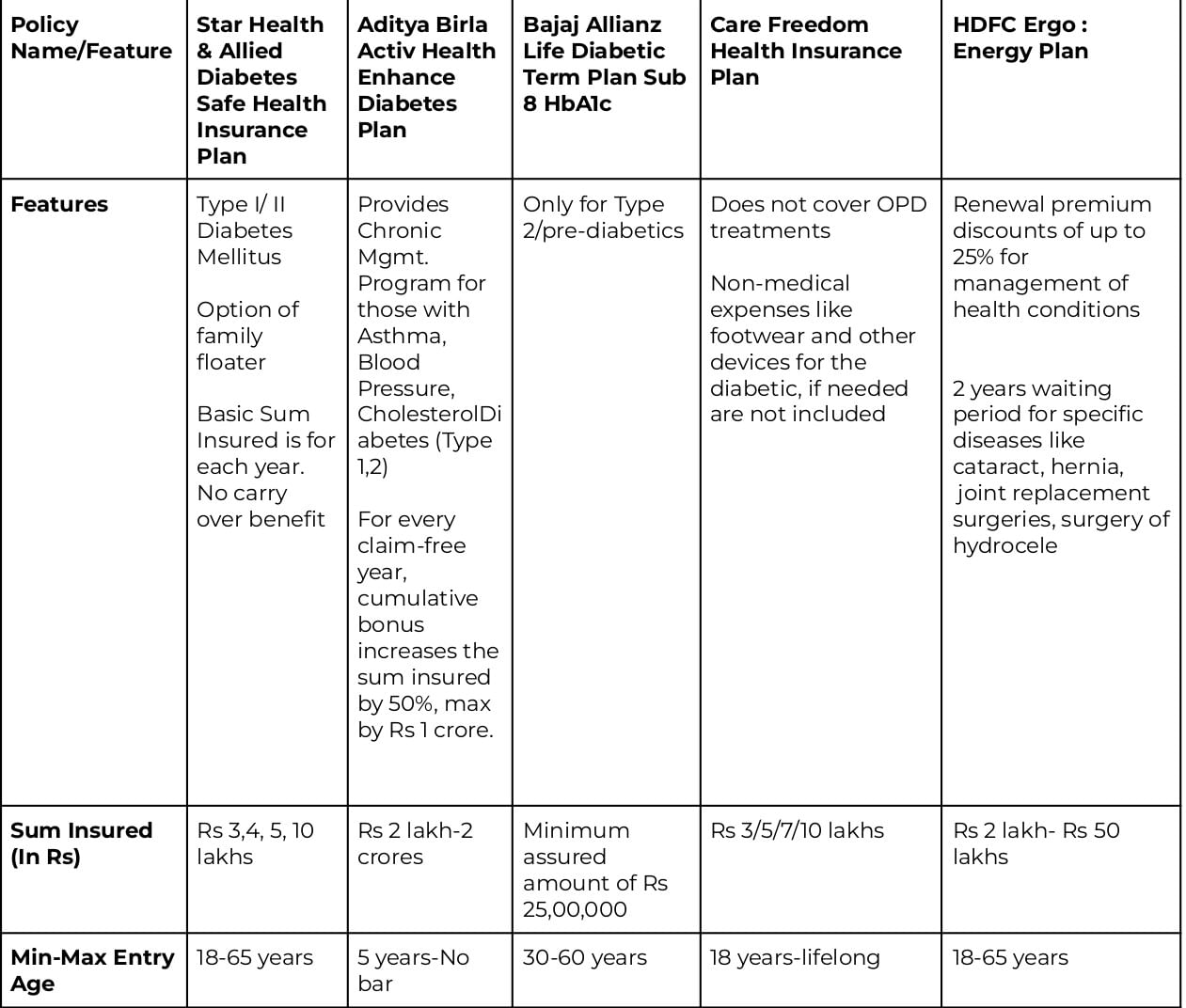

Currently, there are only 4-5 policies that cater specifically to the diabetics. While they may offer better coverage as compared to general health insurance policies, they come with a higher premium payable.

India is rapidly becoming the diabetes capital of the world. A recent study by ICMR (Indian Council of Medical Research) highlighted that India is currently home to 101 million diabetics. India also has a high number of pre-diabetics. About 15.3% of the population, or 136 million people already have abnormally high sugar levels.

But despite this, insurance policies have little space for this exponentially growing subset of disorders, which are taking over our lifestyles. And singeing our pockets, too. Take 83-year old, Delhi-based Dattratraya Dhoble, who is a type-2 diabetic, for instance. He spends over Rs 4,000 every month solely on his medicines.

Add to that the cost of insulin, doctor consultations and other medical expenses that are a consequence of diabetes (nerve damage, heart/kidney problems, stroke), and the total cost skyrockets.

The diabetes menace

However, your regular insurance policies might not always cover diabetes, even as a pre-existing disease. And even if they do, you might have to wait years before you can make a claim. While coverage for type-1 diabetes is largely absent, type-2 may be covered under some health insurance policies. However, they might also not be comprehensive, which means you will end up paying most expenses from your pocket.

Currently, there are only 4-5 policies that cater specifically to the diabetics. While they may offer better coverage as compared to general health insurance policies, they come with a higher premium payable.

For instance, the HDFC Ergo Energy plan charges an annual premium of Rs 50,000 for a cover up to Rs 5,00,000, if you’re aged between 46-50. For those aged between 36-45, the premium stands at around Rs 36,000.

And even when you have insurance, you will not be able to utilise the benefits to the full. Most policies have set sub-limits, which means that the insurer won’t be liable to pay you anything under certain heads post a predetermined amount.

For instance, pre and post hospitalization expenses form a big chunk of one’s medical expenditure. The CARE Freedom plan caps this limit to 7.5% of the total hospitalisation expenses. Beyond that, it is your pocket that will end up bearing the brunt.

The reason why India does not have strong insurance coverage for OPD, or even post-hospitalization process is because it is highly fragmented. “People usually go to private practitioners, and not institutional players when it comes to OPD visits. That makes it difficult for insurance companies to standardise the process and hence, the higher number of exclusions. Moreover, the idea of insurance in India is more inclined towards savings, and not comprehensive protection. People buy insurance that offers OPD coverage up to Rs 6,000, even though their actual expenses touch Rs 7,000-10,000”, notes Mahaveer Chopra, founder of Beshak.in

Look out for exclusions

There are many exclusions that might not be covered under the policy. These exclusions, most of the time, are a direct consequence of the disease, and can inflict far more sustained damages to the patient.

For instance, the CARE plan does not include OPD visits, routine eye/dental checkups, external devices that might be needed by the diabetic like footwear, walkers, ambulatory devices and more.

Diabetes can seriously damage, even permanently blind the patient, while also damaging nerves, which might result in foot amputation or impairment, dental issues. These are significant expenses the patient might end up bearing from his own pocket, despite having insurance.

That’s why Vivek Chaturvedi, CMO and Head of Direct Sales, Digit General Insurance advises people to opt for a comprehensive health plan. “A comprehensive plan covers medical expenses for illnesses related to hospitalization, day care procedures, pre- and post-hospitalization expenses, organ donor expenses, among others. Hence, having a comprehensive cover may not necessitate a need to specifically seek out disease-specific covers for lifestyle ailments. However, do note that they may have a waiting period of 2-4 years for pre-existing diseases and specific illnesses.

But, if you are somebody who is finding it difficult to get any type of comprehensive health insurance due to your age or say existing severe ailment, and have a family history of that specific disease, one can look at such disease-specific covers”.

But the caveats associated with such policies are far too many, says Chaturvedi. “Keep in mind that such disease-specific covers may come with their own eligibility criteria based or recency or severity of the condition, sub-limits and may also have a conditional waiting period, which the insurer may impose at its discretion. Waiting periods for all other types of PEDs and specific illnesses may also be applicable. This may limit people with severe conditions from getting such covers, thus not offering any additional advantage”.