LIC’s SIIP: This unit linked policy can pay you Rs70 lakh on maturity

If a 30-year-old invests Rs 30,000 quarterly in LIC's SIIP for 25 years, then on maturity the policy will return Rs 69.17 lakh assuming an 8% return

Life Insurance Corporation’s SIIP is a unit-linked insurance plan, which offers protection as well as investment benefits throughout the term of the policy. Unlike traditional plans, the policy gives you four investment options for allocating your funds between equities and debt, as per your risk profile. Moreover, the policy pays you guaranteed additions up to 25% for holding the policy till maturity.

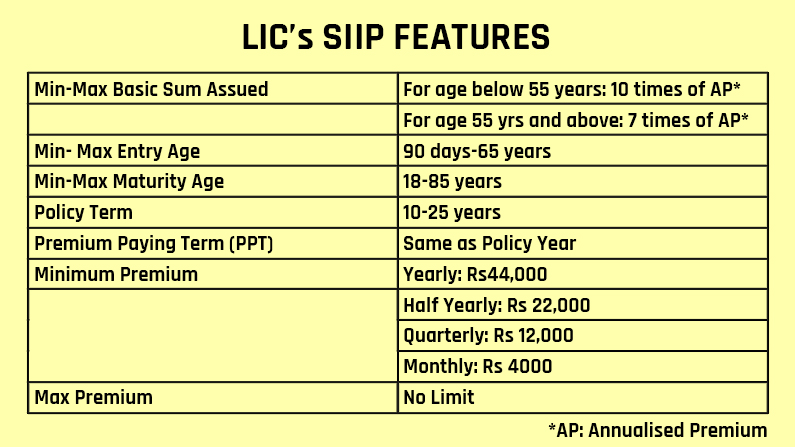

Features

It is a regular premium policy where premiums are paid every year at yearly, half-yearly, quarterly, or monthly mode, according to your convenience. If the payment date is missed then a grace period of 15-30 days is allowed depending on the payment mode. The table below lists other features of the plan:

Charge structure

New age ULIPs are very cost-effective, compared to old plans where allocation charges were as high as 70-90% for the first year. The LIC’s SIIP policy deducts charges under the three heads as follows:

Premium allocation charge: Premium allocation charges for 1st year is 8% (3% for online mode), for 2nd to 5th year it is 5.5% (2% for online mode) and from 6th year onwards it is 3% (1% for online mode.)

Mortality charges: It ranges between Rs 1.25 to Rs 14.42 per thousand depending on your age between 25 and 60 years.

Fund Management Charges: 1.35% per annum for all the four fund options

Performance

On maturity, the fund value is paid to the policyholder. Apart from the fund value it also refunds the total amount of mortality charges deducted during the term of the policy. For example, if a 30-year-old invests every quarter Rs 30,000 in the policy for the term of 25 years, then the policy will return Rs 40.04 lakh and Rs 69.17 lakh at an assumed return of 4% and 8%. The net yield works out to Rs 6.43% for the gross return of 8%. The basic sum assured is assumed at Rs 12 lakh. Here you have to remember that being a market-linked policy your actual return can be higher or lower than the assumed rate of 8%.

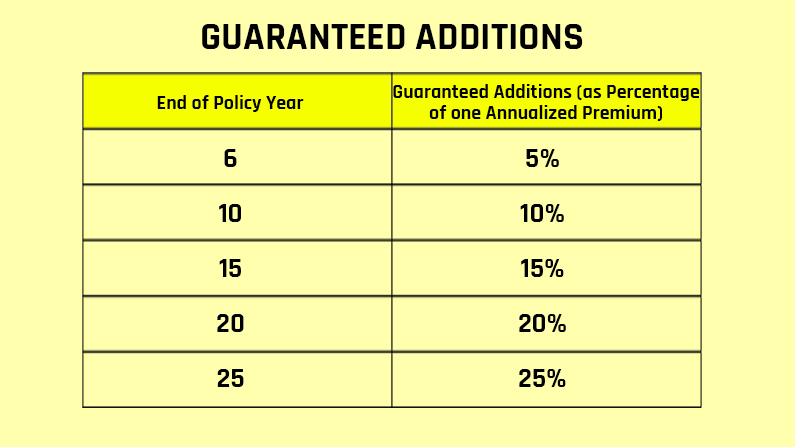

Guaranteed additions

A policyholder is also paid guaranteed additions depending on the number of years of completion of the policy:

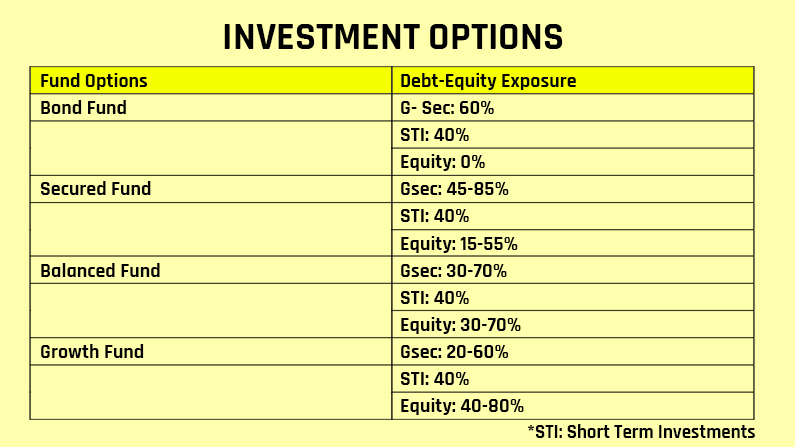

Investment options

A policyholder has the choice of investing in these four funds depending on how much equity exposure one wants to have in the policy. There are four funds to choose from:

Partial withdrawals

The policyholder can partially withdraw after the fifth year provided all due premiums have been paid. A nominal Rs 100 is deducted on partial withdrawal. For example, from 6th to 10th year one can withdraw up to 20%, from 11th to 15th year up to 25%, from 16th to 20th year up to 30% and after 21st year one can withdraw up to 35%.

Early exit

A policyholder can exit from the policy after the completion of 5 years. Before 5 years discontinuance charges are levied in the range of Rs 1,000-Rs 6,000 depending on the year and the premium amount.

Death benefit

If the policyholder dies during the tenure of the policy then an amount equal to the highest of the following gets payable:

1. Basic sum assured

2. Fund value

3. 105% of the total premiums received up to the date of death

If age is less than 8 years: In case the life assured is less than 8 years, the insurance cover will commence either on the completion of 2 years or on policy anniversary coinciding with immediately following the completion of 8 years of age, whichever is earlier. The policyholder can also opt to receive the death benefit in installments.