Starting your first job? Here’s a complete tax guide

Here's your complete tax guide that can help you begin your tax filing journey with utmost clarity and ease

Every day is a new beginning. Once people complete their studies, they are super excited about the possibilities that lie ahead. Whether you get your dream job or not, taxes are going to haunt you as soon as start earning. Many people believe that if they have the PAN, they must file an income tax return. But the interaction with the Income-tax department generally starts when you commence your earnings. So if you’ve started earning, make sure to take care of your taxes as you’re always under the scanner of the Income-Tax department.

The first important step is to collect Form 16 from your employer. You need to give the details of your taxable income by filing the Income-tax Return. To file the Income-tax return you need to obtain Form 16 from the employer and create an account at the e-filing portal to file your Income-tax return.

Here’s your complete tax guide that can help you begin your tax filing journey with utmost clarity and ease.

Understand your salary structure

Salary includes wages, pension, gratuity, fees, advance salary, leave encashment, etc. The employer as per the terms of employment may provide various allowances to the employees. An allowance is generally taxable unless it is specifically exempted from tax.

“The employees are liable to pay tax on salary on a due or receipt basis, whichever happens, earlier. Salary due from an employer in the previous year, even if it is not yet paid, is still chargeable to tax. The expression ‘due’ implies that there is an obligation on the part of the employer to pay that amount and a right has accrued to the employee to claim the same. Thus, the salary gets taxed in the hands of an employee even if it is not received by him,” said Tarun Kumar, chartered accountant & direct tax leader at Coherent Advisors.

The employee can check the detailed break-up of monthly salary in the salary slip. You may plan your tax savings if you carefully analyse your salary structure. For example, you may claim exemption of house rent allowances if you pay rent for the accommodation. If you go on vacation, leave travel concession can be claimed.

Deduction from salary

Salary is chargeable to tax on a gross basis. In general, no deduction is allowed while computing the salary income. However, Standard Deduction, Professional Tax and Entertainment Allowance are allowable as deductions while computing the salary income. The standard deduction of Rs 50,000 is allowed from an income taxable under the head salary. The benefit of the standard deduction is available only in cases where the income is taxable under the head salaries.

It must be noted here that you should not claim any deduction which isn’t reflecting in Form 16 and you aren’t eligible to claim it either. Taxpayers often claim fake deductions or inflate existing deductions to reduce their Income-tax liability or to claim refunds. These fake deductions might lead you to trouble.

Alternative Tax Regime

Individual taxpayers have an option to opt for an alternative tax regime. If the option is exercised, the assessee shall not be able to claim specified deductions and exemptions. The assessee opting for the new regime shall be liable to pay income tax at the lower tax rates.

“The alternate tax regime is beneficial to taxpayers or not will depend from person to person and it will depend upon the aggregate amount of deductions/exemptions to which the taxpayer is eligible to claim. The option to opt for alternative tax regime shall be exercised for every previous year where the taxpayer has no business income, and in other cases, the option once exercised for a previous year shall be valid for that previous year and all subsequent years,” Kumar asserted.

If you intimate the employer about your intention to opt for a new tax regime, the employee’s estimated tax liability will be computed as per section 115BAC. Such estimated tax liability is deducted from the employee’s salary on monthly basis throughout employment.

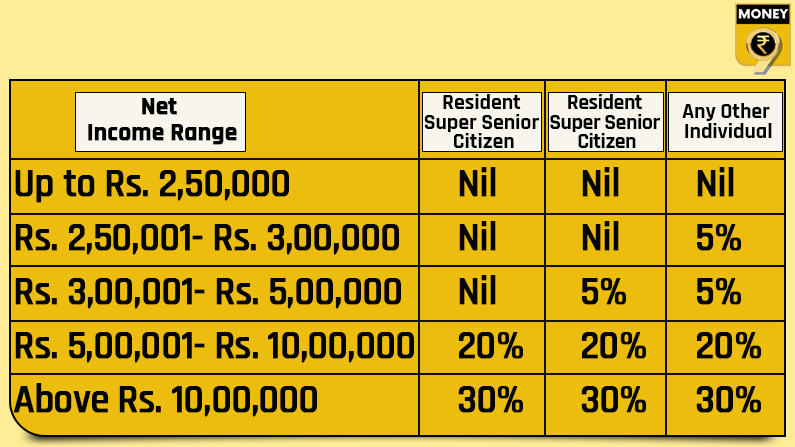

Rate of Tax

According to Kumar, an individual is not liable to pay tax if his normal income is up to the maximum exemption limit. The basic exemption limit and the tax rates in the case of an individual depend upon his age during the relevant previous year. The normal tax rates for individual are depicted in the table below.

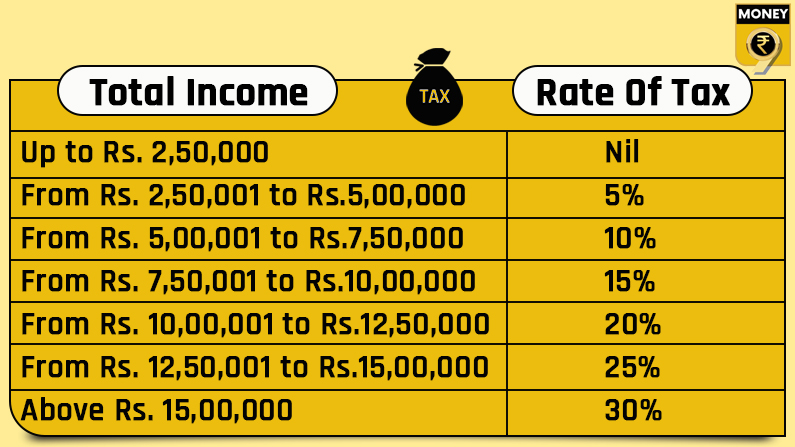

An individual can also opt for alternative tax regime, the rate of tax as applicable to person option for alternative tax regime shall be as under:

Plan your investments

If you make investments, you can substantially reduce your tax liabilities. The payment for insurance policies, repayment of housing loan, repayment of education loan, medical insurance policies reduce your income tax liability. Apart from that, you may also make investments in mutual funds, PPF and tax saver fixed deposits etc.

“For persons starting their first job, often liquidity is more important. In such a situation, they may also need to see which tax deduction investment option has a minimum lock-in period. Viz. ELSS has lock in of only 3 years, Bank term deposits have a lock in of 5 years, whereas PPF has lock in of 15 years. ULIPs also have lock-in period of different duration starting 5 years to 15-20 years depending on the plan taken by the person,” said Shailesh Kumar, partner at Nangia & Co LLP.

He further added, “Someone looking to diversify their earnings, can either invest in fixed return term deposits or invest in Equity-linked savings schemes. The person may either invest in term insurance or a unit-linked insurance policy, medical insurance policy, etc. The investment options available under 80C, 80D, 80G, etc. may actually the taxpayer reach a lower or nil tax slab bracket, in addition to generating future financial and social security benefits.”

Meanwhile, Tarun pointed, “If you have not submitted your investment proofs to your employer, you can still claim tax deductions. You can claim all eligible deductions even if these were not considered by the employer and aren’t reflecting in Form 16.”

Deduction of TDS

Tax is deductible on salary if it exceeds the maximum exemption limit which is not chargeable to income tax. The tax from your salary shall be deducted at the time of payment on a monthly basis.

At the time of payment of salary, Kumar explained, “The employer withholds some amount towards the TDS liability and deposits it with the Income-tax department on your behalf before the prescribed due dates. The employer calculates the estimated tax liability of the employee on his salary income. Such estimated tax liability is deducted from the employee’s salary on monthly.”

In the last quarter of the financial year, the employer will ask you to submit proof of investments. These proofs shall be compared by the employer with the declaration you had submitted at the beginning of the year and any deficiency in the two figures shall result in a higher deduction of TDS from the salary.

Change in job during year

If you have changed the job during the year, then do remember to report the salary income earned from both the employers. It is also likely that there would be a deficit in the tax liability and tax deducted by the employers. Therefore, pay the taxes before the filing of the return.

Fee for delay in filing of the ITR

If a taxpayer, who is required to furnish return of income, fails to furnish it by the due date he shall be liable for payment of fee of Rs. 5,000. However, if the total income of the assessee does not exceed five lakh rupees, the fee payable is one thousand rupees.

Also a quick tip from Kumar, “Make sure you submit PAN to the employer, otherwise, the tax shall be deducted at the slab rates or 20%, whichever is higher.”

Download Money9 App for the latest updates on Personal Finance.